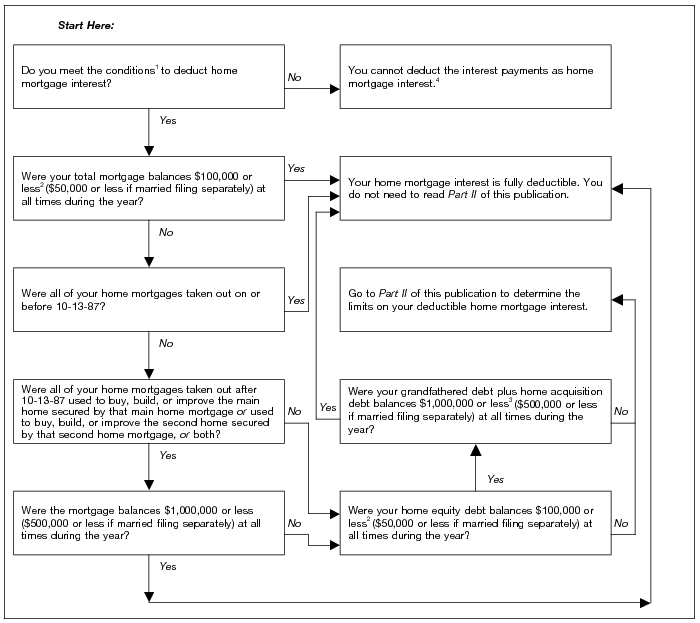

The Tax Consequences of Mortgage Debt Cancellation

In 2007, the Mortgage Forgiveness Debt Relief Act was passed and, believe it or not, the IRS is now doing everything it can to help Americans take advantage of the law to save money on their taxes. And with (the new deadline) April 17 just around the corner, this campaign could not be more timely.

After reviewing the results of a rudimentary survey on the subject, I was shocked at the level of misinformation surrounding mortgage debt cancellation. A handful of respondents were completely unaware of this Act and assumed either that they would be taxed on their cancelled debt. Others were equally unaware of the Act but had otherwise assumed that debt cancellation of any kind can always be written off.

Allow me to clear things up: as a result of the law (and its recent extension), taxpayers will not be held liable for up to $2 million in cancelled mortgage debt from 2007 to 2012. This applies principally to short sales and foreclosures on underwater mortgages, as well as to borrowers whose mortgage debt was cancelled (or not!) due to bankruptcy or insolvency. That’s not to say that any losses associated with foreclosure or short sales can be deducted from income (a major difference!), but rather excluded (not subject to taxes).

There are a couple of qualifications that I want to mention. First, only $1 million in cancelled mortgage debt can be excluded if filing separately. In addition, the cancelled debt must be associated with a primary residence, and not for a vacation home, rental property, or business property. In addition, home equity debt is eligible for the exclusion, but only insofar as it was used for renovation or other home-related expenditures, and not to pay down credit-card debt, for example. [It should be noted that credit card debt and other loans can also be excluded if the cancellation is associated with a title 11 bankruptcy case or insolvency].

If your lender can cancelled more than $600 of mortgage debt, it is required by law to have sent you a 1099-C form by February 2, with the amount of cancelled debt and the fair market value of any foreclosed property clearly indicated. If you haven’t received this form or disagree with any of the figures, you are advised to contact your lender immediately. Otherwise, simply copy the numbers over to IRS Form 982 (Reduction of Tax Attributes Due to Discharge of Indebtedness) and file it with the other forms when preparing your taxes.

Bear in mind, finally, that this debt cancellation is the result of a special policy (due to extenuating circumstances) and you should expect that after 2012, the tax treatment of cancelled mortgage debt will revert back to normal. In other words, it will be taxed as ordinary income. This is something that you might want to consider if your mortgage is underwater and you are weighing your options.

For more information, you can consult the full IRS entry on the tax treatment of cancelled debt. If you are having trouble resolving a tax issue, you can contact the Taxpayer Advocate Service.