2018 Tax Bill Impact on Homeowners & Mortgage Interest Deduction

The new Tax Cuts and Jobs Act tax bill which will go into effect on January 1, 2018 is expected to be signed into law in the next two weeks.

Here are some of the highlights of how the bill will impact homeowners.

Mortgage Interest Deduction

Interest on loans for purchasing first or second homes is deductible. The mortgage debt eligibility cap was lowered from $1 million to $750,000.

Homeowners which have mortgages in place by December 31, 2017 will be grandfathered into the old $1 million cap.

in the case of taxable years beginning after December 31, 2017, and beginning before January 1, 2026, a taxpayer may treat no more than $750,000 as acquisition indebtedness ($375,000 in the case of married taxpayers filing separately). In the case of acquisition indebtedness incurred before December 15, 2017 this limitation is $1,000,000 ($500,000 in the case of married taxpayers filing separately). For taxable years beginning after December 31, 2025, a taxpayer may treat up to $1,000,000 ($500,000 in the case of married taxpayers filing separately) of indebtedness as acquisition indebtedness, regardless of when the indebtedness was incurred.

At a current mortgage interest rate of 4.10% on jumbo mortgages this would equate to a maximum deduction of $30,750 on a new $750,000+ mortgage.

Mortgage refinancing will retain interest deductibility & homeowners who were grandfathered in before the new law will keep the grandfathered status, even if they refinance after the new law goes into effect.

Special rules apply in the case of indebtedness from refinancing existing principal residence acquisition indebtedness. Specifically, the $1,000,000 ($500,000 in the case of married taxpayers filing separately) limitation continues to apply to any indebtedness incurred on or after November 2, 2017, to refinance qualified residence indebtedness incurred before that date to the extent the amount of the indebtedness resulting from the refinancing does not exceed the amount of the refinanced indebtedness. Thus, the maximum dollar amount that may be treated as principal residence acquisition indebtedness will not decrease by reason of a refinancing

Here are more specifics on the grandfathering clock

The conference agreement provides that a taxpayer who has entered into a binding written contract before December 15, 2017 to close on the purchase of a principal residence before January 1, 2018, and who purchases such residence before April 1, 2018, shall be considered to incurred acquisition indebtedness prior to December 15, 2017 under this provision.

Interest on HELOCs & Home Equity Loans

Interest on a HELOC or home equity loan is no longer tax deductible unless the debt is considered origination debt, which would require the debt be used to pay for building or substantially improving a property.

under the provision, interest paid on home equity indebtedness is not treated as qualified residence interest, and thus is not deductible. This is the case regardless of when the home equity indebtedness was incurred.

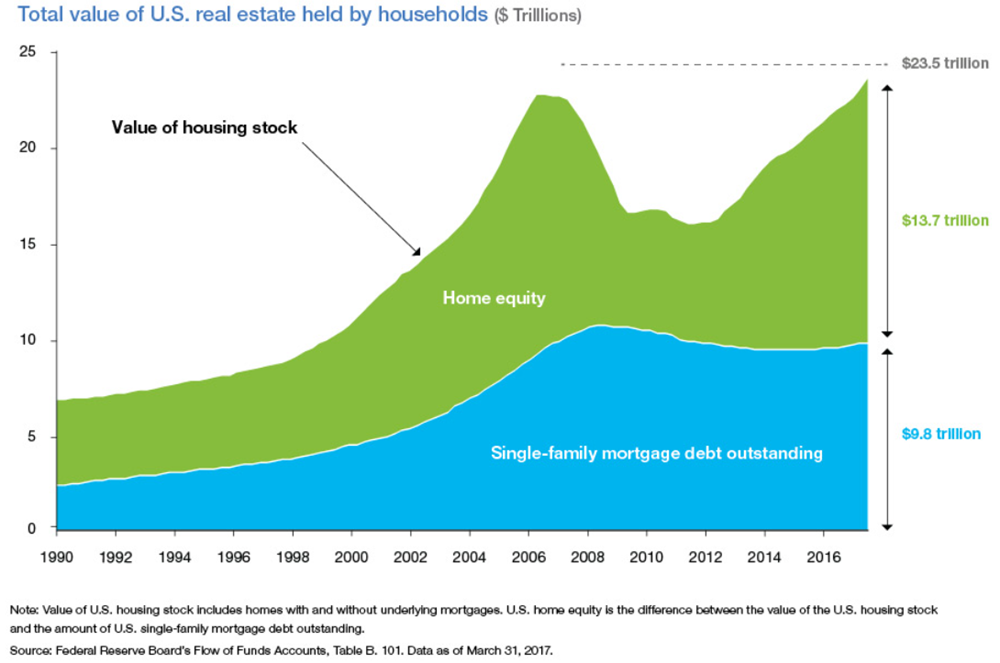

Homeowners have built up significant home equity since the housing price crash nearly a decade ago. Mortgage debt is up only modestly over the past few years after declining throughout most of the housing & economic recovery.

TransUnion put out a report in October where they suggested 10 million borrowers will take out a HELOC between 2018 and 2022.

The TransUnion HELOC study found that rising home prices and the resulting increase in equity is beginning to fuel interest in HELOCs. The Case-Shiller home price index rose as high as 180 in 2005 and 185 in 2006 before dropping to 134 in 2012. By July 2017 it had risen again to 194, and is expected to rise in the next few years to well over 200.

“While HELOC originations often track with home equity, which is correlated to rising home prices, we found that the rebound in HELOCs diverged from the recovery in home values following this past recession,” said Mellman.

Mortgage refinancing dipped from about 48% of the market in 2016 to 33% of the market this year. It is expected to fall further to 25% of mortgage originations next year. With tight home supplies home equity lines were expected to be one of the few areas of growth across the industry. It remains to be seen if this shift in tax treatment will impact the growing HELOC demand.

Income Tax Brackets

| Tax Rate | Married Filing Jointly | Head of Household | Single Filers |

|---|---|---|---|

| 10 percent | $0 to $19,050 | $0 to $13,600 | $0 to $9,525 |

| 12 percent | $19,050 to $77,400 | $13,600 to $51,800 | $9,525 to $38,700 |

| 22 percent: | $77,400 to $165,000 | $51,800 to $82,500 | $38,700 to $82,500 |

| 24 percent: | $165,000 to $315,000 | $82,500 to $157,500 | $82,500 to $157,500 |

| 32 percent: | $315,000 to $400,000 | $157,500 to $200,000 | $157,500 to $200,000 |

| 35 percent: | $400,000 to $600,000 | $200,000 to $500,000 | $200,000 to $500,000 |

| 37 percent: | $600,000 and above | $500,000 and above | $500,000 and above |

Standard Deductions

| Deduction & Exemption Type | Current | Proposed Law |

|---|---|---|

| Single Standard Deduction | $6,350 | $12,000 |

| Married Standard Deduction | $12,700 | $24,000 |

| Personal Exemption | $4,050 | $0 |

| Child Tax Credit | $1,000 | $2,000 |

Currently the child tax credit begins phasing out at $110,000. The proposed bill would lift the phase-out to $400,000. Other dependents who are not children also provide a $500 credit.

State & Local Tax Deduction

Deduction capped at a maximum of $10,000 of some combination of property tax along with either income or sales tax.

The combination of lowering the cap on mortgage interest & limiting SALT deductions could have a significant impact on some expensive real estate markets in high tax areas. An article in the Wall Street Journal stated:

Limiting those state and local tax deductions, home prices in Manhattan could fall as much as 9.5%, according to an analysis by Moody’s Corp.

Obamacare Individual Mandate

Penalty for not carrying health insurance repealed.

Fire & Flood Losses

Only considered deductible if they happen during an event the president officially declares to be a disaster.

Moving Expenses

While some military members will still be able to deduct moving expenses, most people will no longer be able to do so.

Capital Gains on Home Sales

No major changes. Married couples can exclude up to $500,000 on a home sale so long as it was their primary residence for 2 or more of the past 5 years. Individuals can exclude up to $250,000.

Alimony

Divorcees who pay alimony will have to pay tax on the income, while those receiving the alimony will no longer be required to pay income taxes on the funds. This change will go into effect in 2019.

El Monte Homeowners May Want to Refinance While Rates Are Low

US 10-year Treasury rates have recently fallen to all-time record lows due to the spread of coronavirus driving a risk off sentiment, with other financial rates falling in tandem. Homeowners who buy or refinance at today's low rates may benefit from recent rate volatility.

The following table shows current 30-year mortgage refinance rates available in El Monte. You can use the menus to select other loan durations, alter the loan amount. or change your location.

Leave a Reply

Free Mortgage Calculator for Your Website!

Would your customers benefit from a free mortgage calculator on your website? Learn how to add a calculator to your website in less than a minute - FREE!