Federal Reserve Lowers Fed Funds Rate Twice on Coronavirus Fears

The Impact of Fear on Economic Activity

When people are fearful they tend to cut back on consumption outside of fear-based purchases like toilet paper, cleaning supplies, face masks, guns and gold. If the fear is widespread enough financial asset prices can sell off, further boosting fear, leading to a doom loop cycle where the financial abstractions of the economy lead the real economy lower as the opposite of the wealth effect takes place.

How Big is Travel?

Travel and hospitality account for about 15% of the domestic economy. Many other businesses like bars & restaurants are shut down or only allow to-go orders.

The United States has run a large and growing goods trade deficit with China for decades. Chinese students attending universities and Chinese tourism have been strong services exports for the United States. Airplanes manufactured by Boeing are also a large export.

The Federal Reserve Fights Back

The Federal Reserve has moved to try to offset some of the adverse impacts of COVID-19.

- On March 3, 2020 the Federal Reserve Open Market Committee (FOMC) lowered rates from 1.75% to between 1% to 1.25%.

- Last Sunday the Federal Reserve slashed the federal funds rate by a percent down to 0.00% to 0.25%, making their March 15 cut the second emergency rate cut in 13 days.

- On Sunday the Federal Reserve also announced $700 billion worth of quantitative easing, with $500 billion going toward Treasurys and $200 billion going toward mortgage-backed securities.

The goal of these moves is to lower the hurdle rate for investments while lowering the carrying cost of debt for companies and flooding the market with liquidity to offset forced position liquidations caused by the crisis.

Does the Federal Reserve Control Mortgage Rates?

The Federal Reserve controls the short end of the yield curve, but the longer end of the yield curve has been falling throughout the year as well on coronavirus-driven recession fears.

The longer end of the curve is controlled in part by inflation expectations along with factors like liquidity and the balance of fear versus greed in the capital markets.

- If investors perceive risk to be low they generally prefer to invest in higher returning equities over lower returning bonds.

- If investors perceive risk to be high they prefer shorter-duration high-quality liquid bonds to more speculative equities.

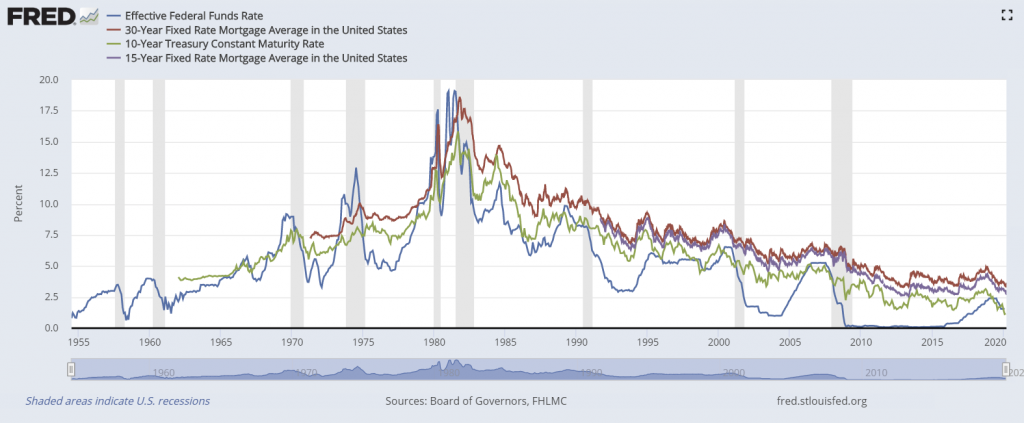

The 30-year fixed rate mortgage tends to track the 10-year Treasury at a slightly higher yield. The following FRED graph shows how both the 15-year & 30-year fixed-rate mortgage rates closely track the 10-year Treasury versus the Fed Funds rate.

In spite of loans being offered for 30 years, many people move homes or refinance their loans roughly every 7 to 12 years, making the 10-year a better duration match for the typical mortgage than the 30-year Treasury Bond.

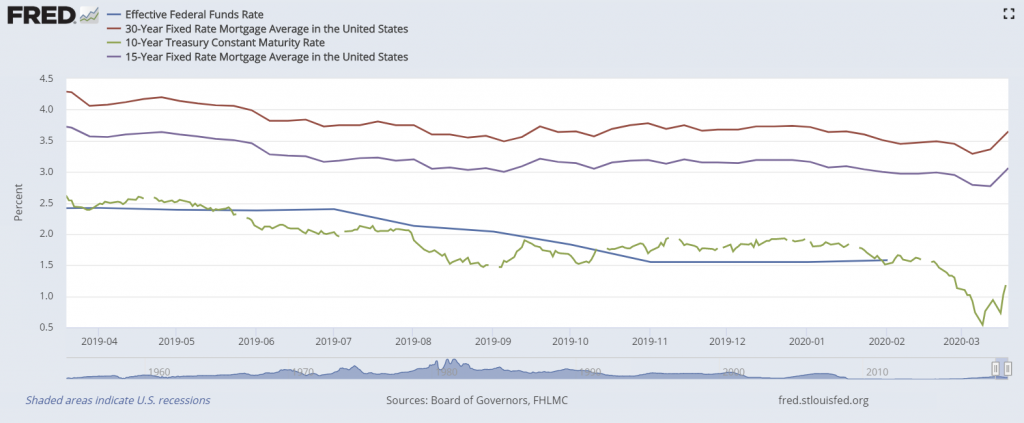

Zooming in more closely on the graph you can see how in recent weeks as government stimulus measures worked their way through Congress both the 10-year and mortgage rates shot up, even as the FOMC dropped the Fed Funds rate to 0.0% to 0.25%.

Increased fiscal stimulus lowers the risk of a deep recession & increases inflation expectations, this can in turn cause bonds to sell off, boosting their yields.

| Rate Type | 1-9-20 | 3-5-20 | 3-19-20 |

|---|---|---|---|

| Fed Funds Rate | 1.75% | 1-1.25% | 0-0.25% |

| 10-Year Treasury | 1.85% | 0.92% | 1.18%* |

| 15-Year Fixed Mortgage | 3.07% | 2.79% | 3.06% |

| 15 MRT vs 10 yr Treas. | +1.22% | +1.87% | +1.88% |

| 30-Year Fixed Mortgage | 3.64% | 3.29% | 3.65% |

| 30 MRT vs 10 yr Treas. | +1.79% | +2.38% | +2.47% |

*data from 3-18-20

As shown in the table above, mortgages trade at around 1.5% to 2.5% higher yields than the 10-year Treasury. Purchasing mortgage-backed securities should tighten this spread by driving down the yields on MBS, which should lower interest rates on mortgages.

This process has pipeline effects which take time to work their way through the economy. At the end of April Freddie Mac’s data showed the 30-year reached a record low of 3.23% and the 15-year dropped to 2.77%.

While there are multiple related layers of uncertainty and volatility in the market, rates may decouple from the 10-year:

Uncertainty surrounding the coronavirus outbreak has bred volatility in mortgage rates. The usual indicators of where rates are headed — namely the yield on the 10-year Treasury — are no longer reliable predictors. Instead, what is having a greater effect on mortgage rates is the capacity of lenders to handle the huge volume of refinances brought on by lower rates and the increasing amount of mortgage-backed securities the Federal Reserve is buying.

How do Homeowners React to FOMC Rate Moves?

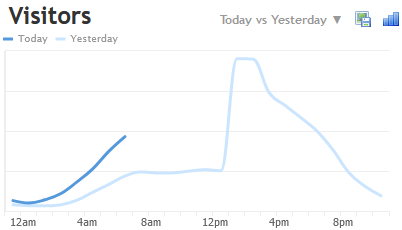

Over the years numerous surveys have shown roughly a quarter to a third of homeowners do not know what their mortgage rate is. While many homeowners do not know what their rate is, Federal Reserve moves are widely covered in the news. This leads to a surge in consumer demand. The following picture shows traffic to this website. The light blue line shows a huge spike on a Sunday after the Federal Reserve announcement.

People who are consumed by fear or worried they may lose their job will be less likely to take on large sums of debt or make bit life choice changes, thus when there is major volatility and uncertainty people are less likely to buy a home using credit. Roughly 88% of residential homes purchased by homeowners are purchased using financing.

Those who already own homes see news of decline in market rates and quickly check to see how much money they can save. As of the end of March the MBA recently stated that refinance volume has increased in share to where it now represents 75.9% of total mortgage applications.

How is the Mortgage Market Structured?

Individual home loans created by lenders can be held in their company portfolio or can be sold off into the secondary market. Before selling loans off into the secondary market lenders group them into a mortgage-backed security.

Government sponsored entities (GSEs) Fannie Mae and Freddie Mac guarantee MBS which contain conventional mortgages. The Department of Veterans Affairs guarantees VA loans while the USDA guarantees some rural loans and the FHA helps lower risk on some loans issued to low-income homeowners and other groups.

Historically most of the mortgage loan origination market has been dominated by large banks like Wells Fargo, Citigroup, Bank of America, U.S. Bank, and J.P. Morgan Chase. Due in part to regulations enacted after the Great Recession in recent years banks originated around half of home loans while the other half of home loans are originated by firms specializing in mortgage loans like Quicken Loans, PennyMac, Caliber, United Wholesale, Amerihome, loanDepot and Freedom Mortgage.

More recently the nonbank lenders have represented 66% of loan originations according to the Urban Institute. This is a jump from 40% in 2013.

When the mortgage market was dominated by large financial institutions they could easily pull employees across from other departments to service shifts in consumer demand. The streamlined mortgage-focused companies do not have the spare capacity which is created by being part of a larger organization. This means when rates drop the spike in consumer demand causes many lenders to pull back on their marketing spend and rework their existing book of loans to try to get prior borrowers to refinance.

In some cases this means a lender which is at capacity might pause their ad spend and/or lift their advertised rate shown on third party mortgage rate tables to try to discourage incremental consumer demand until the firm is able to hire more employees or the spike in demand dissipates.

On March 6th, Quicken Loans CEO Jay Farner stated:

In the last week, we’ve probably had three record days. Yesterday was, again, a new record for mortgage applications. It really is one of those once-in-a-lifetime opportunities. I’m not certain we’ll see rates like this again.

The conventional loan market still remains robust due to the backing of the GSEs and the United States Federal Government. That being said, the jumbo mortgage market does not have this backing & is much more likely to see volatility. Wells Fargo was the biggest originator of jumbo loans in 2019. They announced they would stop purchasing jumbo loans made by third-party mortgage bankers and they would only refinance existing jumbo loans for customers who hold at least $250,000 in liquid assets with the bank.

Further, some investment firms facing investor redemptions as equities slide are becoming forced sellers of bonds including mortgage bonds and other commercial mortgage paper tied to real estate investment trust (REITs).

“Real estate billionaire Tom Barrack said the U.S. commercial-mortgage market is on the brink of collapse and predicted a “domino effect” of catastrophic economic consequences if banks and government don’t take prompt action to keep borrowers from defaulting. … Specifically, his paper highlights the fragility of mortgage real estate investment trusts, or REITs, and credit funds and the lenders that provide them with liquidity via repurchase financing.”

The standard vanilla mortgage market has many piecemeal regulations and supports coming together to offer homeowners relief.

- Fannie Mae & Freddie Mac suspended foreclosures for 60 days.

- FHFA director Mark Calabria is promoting loan forebearance programs which will not hit consumer credit scores as long as homeowners experiencing hardship contact their loan servicer and stick to the terms of the program. He stated GSEs should be fine so long as the crisis lasts 6 to 8 weeks, but suggested backing from the Federal Reserve or Congress would be needed if the crisis lasts significantly longer than that.

- New York Governor Andrew Cuomo issued an executive order urging banks to postpone mortgage payments for 90 days for financially distressed homeowners.

- The mortgage REIT market began seizing up with many REITs suspending dividends and MFA Financial failing to meet a margin call on March 23, 2020. The Federal Reserve announced unlimited QE. The Federal Reserve Bank of New York will buy $50 billion of agency mortgage-backed securities each business day from March 23rd to March 27th.

- Ginnie Mae is providing lender support: “In a statement late Friday, Ginnie said it would help get cash to companies such as Quicken Loans Inc. and Mr. Cooper Group Inc. that expect a wave of missed payments as borrowers lose jobs and income from widespread closures of nonessential businesses, cancellations of public events and orders for people to stay home if possible.”

- The Federal Reserve is likely to step in offering emergency loans to offset missed payments from workers who are laid off. There is no reason to suspect they would do all the above mentioned interventions while skipping this step in the chain. If they do not intervene, many mortgage servicers are likely to go under due to mandatory MBS payments they are obligated to pay while many homeowners are deferring loan payments. Even the much less populous country of Canada has a half-million mortgage deferral requests while many homeowners in the US have been unable to contact their mortgage servicers as phone lines were busy and calls went unanswered.

- On April 23 Treasury Secretary Steven Mnuchin stated nonbank mortgage servicers did not currently provided the level of systemic risk which would justify the creation of a Fed facility

- Some mortgage industry professionals are pushing to increase conforming loan limits to add liquidity to the upper end of the residential housing market.

Mortgage Deferral versus Mortgage Forbearance

Mortgage Deferral

Mortgage deferrals may allow the homebuyer to make a few additional payments at the end of their mortgage payment period or make a slightly larger monthly payment until they catch up with their original amortization schedule. If you miss 3 months it could add 3 monthly payments to the end of your original loan term, or you could pay a couple hundred extra dollars per month with your regular monthly payment.

Mortgage Forbearance

Mortgage forbearance is simply the suspension of foreclosure. This means if you receive a forbearance for 6 months then when that 6 month period has ended you will end up needing to make your traditional monthly payment on the 7th month AND pay for 6 monthly payments you missed at the same time in a lump sum. If your monthly mortgage payment is $2,000 per month then if you have 6 months forbearance you will end up having to make a $14,000 payment in 7 months.

Hundreds of thousands of Americans are already using forbearance:

For the week of March 23 through March 29, caller requests numbered 218,718. That number jumped to 717,577 requests in the following week, according to a Mortgage Bankers Association calculation. Mortgage servicers are required to grant forbearance to any borrower who requests it with no documentation of hardship necessary.

Millions of Americans are expected to tap mortgage forbearance programs. The FHFA’s Mark Calabria estimated 2 million borrowers would seek forbearance while the Urban Institute’s Laurie Goldman suggested a worst-case scenario could see 12 million Americans tap forbearance programs.

By April 15th the low estimate has already been surpassed. Black Knight data showed that more than 2.9 million homeowners (5.5% of those with an active mortgage) are already in forbearance programs.

On April 24th Bloomberg reported Black Knight data showed homeowners seeking to delay mortgage payments increased 17% over the past week to 3.4 million. About 6.4% of borrowers with an active mortgage entered into forbearance programs, up from 2.9 million or 5.5% a week earlier.

Further breaking down the above statistics,

- around 5.6% of the 27.9 million borrowers with loans backed by Fannie Mae & Freddie Mac missed payments

- around 8.9% of the 12.1 million borrowers with loans backed by Ginnie Mae missed payments

- around 5.7% of the 12.9 million mortgages not backed by any government program were in forbearance

The MBA estimated 4 million homeowners were in forbearance programs on May 3, bringing the total up to 7.91% from 7.54% the prior week. These stats were broken down as follows:

- Ginnie Mae – rose week over week from 10.45% to 10.96%

- Fannie Mae & Freddie Mac rose from 5.85% to 6.08%

- private label security and portfolio loans rose from 8.3% to 8.88%

- depository servicers rose from 8.41% to 8.75%

- independent mortgage banks rose from 7.13% to 7.54%

These numbers are up massively off the baseline as only 0.25% of loans were in forbearance on the week of March 2.

The Mortgage Bankers Association reported that at the end of the week of October 11th mortgages in forbearance plans fell to 5.92% of outstanding loans.

Consumers who obtained a 6-month forbearance could renew it for another 6 months, though renewing it requires contacting their loan servicer and requesting renewal.

We have published an in-depth guide covering mortgage deferral and forbearance programs.

When is the Best Time to Refinance?

Mortgage rates recently reached all-time lows, though they may go even lower after the Federal Reserve rate cut news becomes old news and consumers are not overwhelming lenders.

When the Federal Reserve lowers the Fed Funds rate sometimes the associated spike in consumer demand causes lenders to wait a while before lowering their mortgage rates.

An analogy which helps explain the above if when a war breaks out in the Middle East or something disrupts oil flow local gas stations almost immediately raise fuel prices & when oil prices fall gas stations tend to be slower to follow the move down.

Some lenders who have struggled to keep up have been raising rates. MarketWatch reported the recent weekly mortgage rate increase was the largest since November 2016.

There are many counteracting trends and forces driving rate shifts.

- Fear of financial collapse causing capital to leave the stock market and rotate into bonds and money market accounts as stocks sell off.

- Central bank stimulus lowering the risk of financial contagion by putting a bid under both stocks and bonds. In the short run as financial stability is improved and fear subsides this should drive long duration interest rates higher.

- Fiscal stimulus spends money into the economy to support the economy and raise inflation expectations. If both branches of Congress and the presidency go to the same political party 2021 will likely see a massive fiscal stimulus program. This would increase longer duration interest rates.

- Nonbank lenders have a wave of refinance demand from central bank intervention which they do not have adequate staff to handle. This has caused them to hold back on lowering rates as much as they could have and pull back on advertising until they staff up.

- Over time consumer demand will diminish when rates stop falling. Lenders who have increased hiring will see supply and demand come more in balance.

- Layoffs associated with the economic slowdown might make banks want to tighten credit standards to ensure they are lending to borrowers who are not likely to get laid off and default if the economy continues slowing.

- The work from home movement should create massive waves of innovation as well as new company structures as more businesses move online.

Nobody knows what the rates will be tomorrow or next week. If they had certainty on that they could make a lot of money. Recent market volatility has reached record levels with the DJIA increasing or decreasing by 4% a day for 8 consecutive trading days.

Should You Consider Refinancing Your Home?

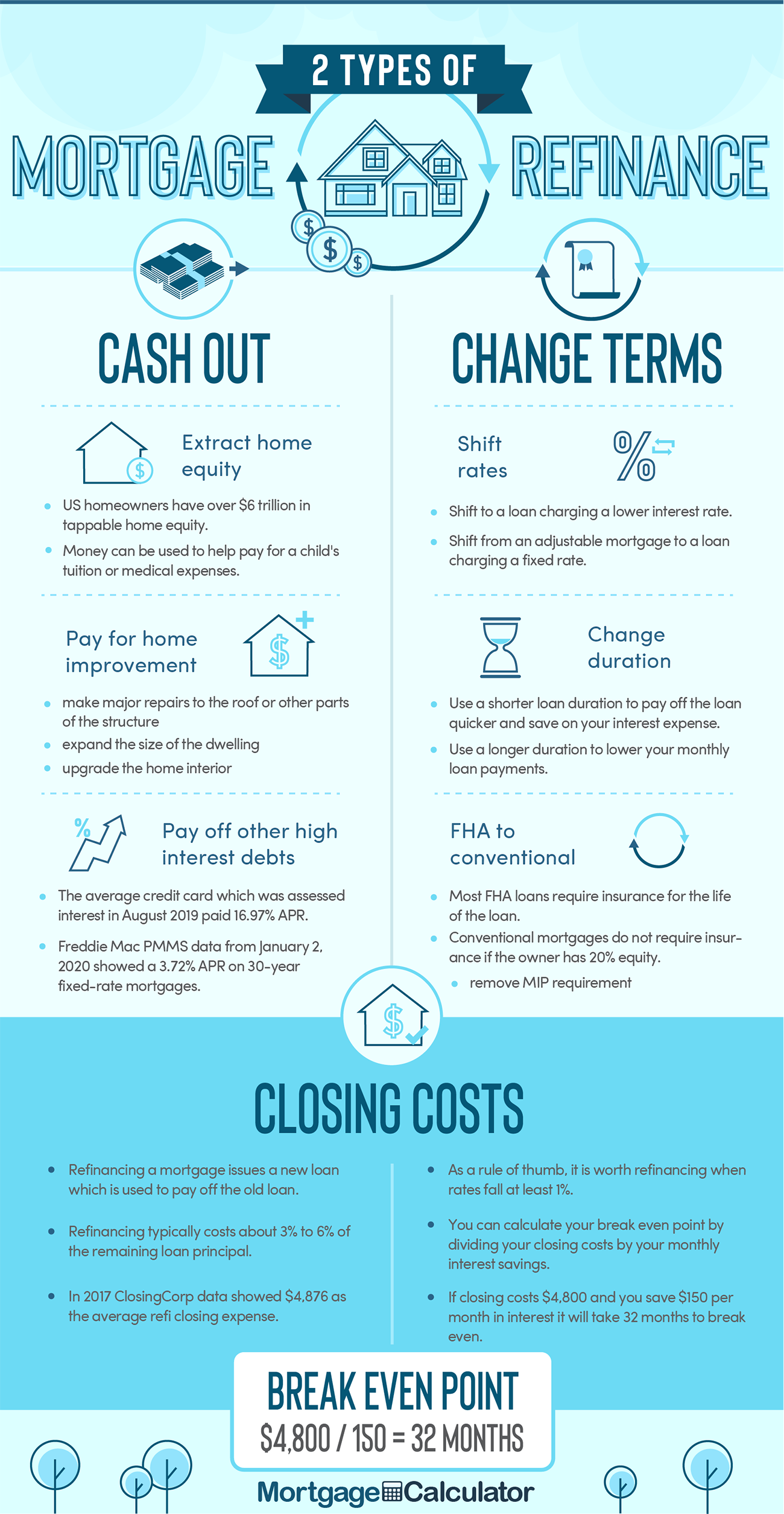

As a general rule of thumb it is worth refinancing if rates fall at least a percent below what you currently pay and you know you are going to live in the home for at least 5 years before moving, selling it, or refinancing again.

Refinancing a home creates a new loan which pays off the old loan. A typical refinance can cost from 3% to 6% of the loan principal. In 2017 ClosingCorp date showed the average refi closing cost to be $4,876.

You can calculate your break even point on refinancing by dividing the closing costs by your monthly interest savings.

A one percent rate decline on a $300,000 loan would save around $2,000 in interest per year.

Some homeowners also choose to refinance not only based on trying to save on interest, but also to cash equity out of their homes. Refinance rates are significantly lower than the rates charged on home equity lines of credit and home equity loans.

Eventually central bank easing and fiscal stimulus will turn financial markets higher and lift inflation expectations, though nobody knows precisely when that will happen.

Which Loan Duration Should I Choose?

Please note that if you reset the term of your loan to a significantly longer duration than what you have remaining on your current loan then you will likely pay more interest over the life of the loan even if your monthly payment falls.

Shorter duration loans typically charge lower interest rates. When you refinance you can lower your total interest expense by ensuring you take out a 10-year, 15-year, 20-year, or 25-year loan which roughly matches the duration left on your current loan instead of refinancing with a new 30-year loan.

While the 30-year mortgage dominates the home purchase market, many homeowners choose to refinance using a 15-year term so they do not reset the clock on their loan and stretch out payments.

The HEROES Act

The HEROES Act established the Emergency Rental Assistance Act and Rental Market Stabilization Act, a $100 billion fund for rental assistance. It also extended the 120-day non-payment eviction moratorium from the CARES Act to a 12-month moratorium. The HEROES Act also created a $75 billion Homeowner Assistance Fund to help homeowners cover property taxes, mortgage payments & utility payments.

The NLIHC covered the HEROES Act provisions in more detail.

The HEROES Act also directed the Federal Reserve to establish an emergency lending facility to residential rental property owners.

Record Year For Mortgage Originations

Urban flight has been caused by the combination of:

- lockdowns taking away many of the entertainment or cultural venues which made higher urban rents worth it

- protests driving safety concerns

- work-from-home requiring more space at home to concentrate & no longer requiring the high rents of a big city where the worker was employed

When the urban flight was coupled with historically low interest rates that has led to what is likely to be a record year for mortgages in 2020 with Fannie Mae suggesting total loan originations will be roughly $4.1 trillion, with refinancing accounting for $2.6 trillion of activity and $1.5 trillion in purchase activity.

Low interest rates and urban flight caused the National Association of Home Builders/Wells Fargo Market Index to reach a record high of 85 in October.

GSE Adverse Market Conditions Fee

Fannie Mae & Freddie Mac announced a 0.5% fee added to home refinancing to account for adverse market conditions. This fee was initially announced in August 12th with intent to begin on September 1, but the fee was later moved to December 1.

This fee should add around $1,400 in costs to the average mortgage refinancing. Loans below $125,000 will not be assessed this fee.

Article Revision History

This article has been revised.

- March 29, 2020: added information about Ginnie Mae providing lenders direct support.

- April 3, 2020: added mortgage refinancing application statistics from the Mortgage Bankers Association.

- April 5, 2020: added notice about new restrictions to jumbo mortgages from Wells Fargo and a section offering a clarification on the difference between mortgage deferral and forbearance.

- April 9, 2020: added recent forbearance stats.

- April 18, 2020: added Black Knight forbearance stats.

- April 24, 2020: updated Black Knight stats.

- April 30, 2020: added reference to new record low mortgage rates based on Freddie Mac data.

- May 17, 2020: added HEROES Act coverage & the latest MBA forbearance stats.

- October 20, 2020: added adverse market conditions fee

2018 Tax Bill Impact on Homeowners & Mortgage Interest Deduction

The new Tax Cuts and Jobs Act tax bill which will go into effect on January 1, 2018 is expected to be signed into law in the next two weeks.

Here are some of the highlights of how the bill will impact homeowners.

Mortgage Interest Deduction

Interest on loans for purchasing first or second homes is deductible. The mortgage debt eligibility cap was lowered from $1 million to $750,000.

Homeowners which have mortgages in place by December 31, 2017 will be grandfathered into the old $1 million cap.

in the case of taxable years beginning after December 31, 2017, and beginning before January 1, 2026, a taxpayer may treat no more than $750,000 as acquisition indebtedness ($375,000 in the case of married taxpayers filing separately). In the case of acquisition indebtedness incurred before December 15, 2017 this limitation is $1,000,000 ($500,000 in the case of married taxpayers filing separately). For taxable years beginning after December 31, 2025, a taxpayer may treat up to $1,000,000 ($500,000 in the case of married taxpayers filing separately) of indebtedness as acquisition indebtedness, regardless of when the indebtedness was incurred.

At a current mortgage interest rate of 4.10% on jumbo mortgages this would equate to a maximum deduction of $30,750 on a new $750,000+ mortgage.

Mortgage refinancing will retain interest deductibility & homeowners who were grandfathered in before the new law will keep the grandfathered status, even if they refinance after the new law goes into effect.

Special rules apply in the case of indebtedness from refinancing existing principal residence acquisition indebtedness. Specifically, the $1,000,000 ($500,000 in the case of married taxpayers filing separately) limitation continues to apply to any indebtedness incurred on or after November 2, 2017, to refinance qualified residence indebtedness incurred before that date to the extent the amount of the indebtedness resulting from the refinancing does not exceed the amount of the refinanced indebtedness. Thus, the maximum dollar amount that may be treated as principal residence acquisition indebtedness will not decrease by reason of a refinancing

Here are more specifics on the grandfathering clock

The conference agreement provides that a taxpayer who has entered into a binding written contract before December 15, 2017 to close on the purchase of a principal residence before January 1, 2018, and who purchases such residence before April 1, 2018, shall be considered to incurred acquisition indebtedness prior to December 15, 2017 under this provision.

Interest on HELOCs & Home Equity Loans

Interest on a HELOC or home equity loan is no longer tax deductible unless the debt is considered origination debt, which would require the debt be used to pay for building or substantially improving a property.

under the provision, interest paid on home equity indebtedness is not treated as qualified residence interest, and thus is not deductible. This is the case regardless of when the home equity indebtedness was incurred.

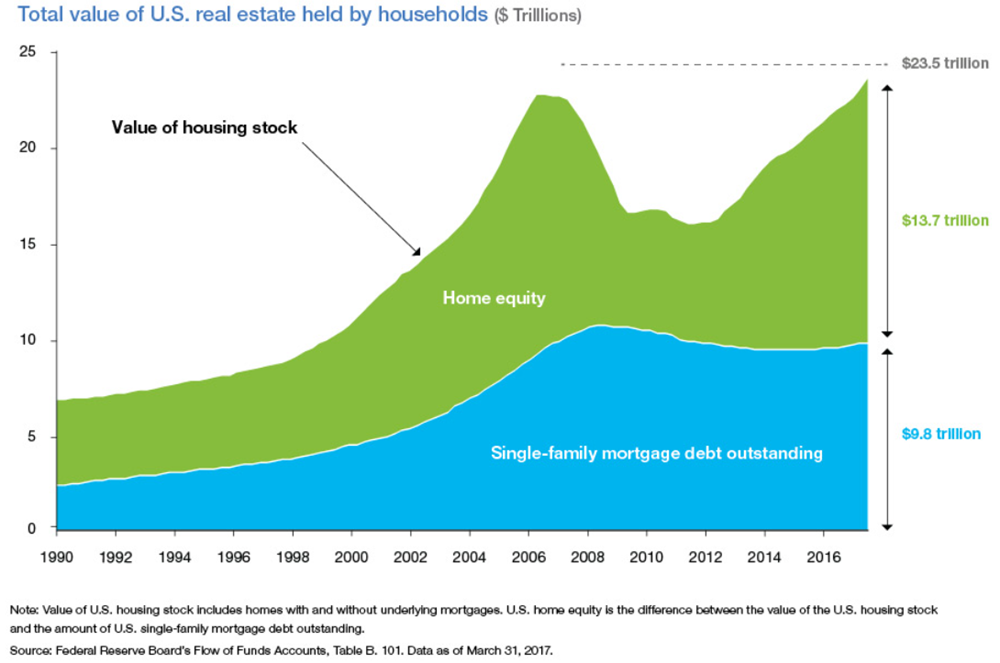

Homeowners have built up significant home equity since the housing price crash nearly a decade ago. Mortgage debt is up only modestly over the past few years after declining throughout most of the housing & economic recovery.

TransUnion put out a report in October where they suggested 10 million borrowers will take out a HELOC between 2018 and 2022.

The TransUnion HELOC study found that rising home prices and the resulting increase in equity is beginning to fuel interest in HELOCs. The Case-Shiller home price index rose as high as 180 in 2005 and 185 in 2006 before dropping to 134 in 2012. By July 2017 it had risen again to 194, and is expected to rise in the next few years to well over 200.

“While HELOC originations often track with home equity, which is correlated to rising home prices, we found that the rebound in HELOCs diverged from the recovery in home values following this past recession,” said Mellman.

Mortgage refinancing dipped from about 48% of the market in 2016 to 33% of the market this year. It is expected to fall further to 25% of mortgage originations next year. With tight home supplies home equity lines were expected to be one of the few areas of growth across the industry. It remains to be seen if this shift in tax treatment will impact the growing HELOC demand.

Income Tax Brackets

| Tax Rate | Married Filing Jointly | Head of Household | Single Filers |

|---|---|---|---|

| 10 percent | $0 to $19,050 | $0 to $13,600 | $0 to $9,525 |

| 12 percent | $19,050 to $77,400 | $13,600 to $51,800 | $9,525 to $38,700 |

| 22 percent: | $77,400 to $165,000 | $51,800 to $82,500 | $38,700 to $82,500 |

| 24 percent: | $165,000 to $315,000 | $82,500 to $157,500 | $82,500 to $157,500 |

| 32 percent: | $315,000 to $400,000 | $157,500 to $200,000 | $157,500 to $200,000 |

| 35 percent: | $400,000 to $600,000 | $200,000 to $500,000 | $200,000 to $500,000 |

| 37 percent: | $600,000 and above | $500,000 and above | $500,000 and above |

Standard Deductions

| Deduction & Exemption Type | Current | Proposed Law |

|---|---|---|

| Single Standard Deduction | $6,350 | $12,000 |

| Married Standard Deduction | $12,700 | $24,000 |

| Personal Exemption | $4,050 | $0 |

| Child Tax Credit | $1,000 | $2,000 |

Currently the child tax credit begins phasing out at $110,000. The proposed bill would lift the phase-out to $400,000. Other dependents who are not children also provide a $500 credit.

State & Local Tax Deduction

Deduction capped at a maximum of $10,000 of some combination of property tax along with either income or sales tax.

The combination of lowering the cap on mortgage interest & limiting SALT deductions could have a significant impact on some expensive real estate markets in high tax areas. An article in the Wall Street Journal stated:

Limiting those state and local tax deductions, home prices in Manhattan could fall as much as 9.5%, according to an analysis by Moody’s Corp.

Obamacare Individual Mandate

Penalty for not carrying health insurance repealed.

Fire & Flood Losses

Only considered deductible if they happen during an event the president officially declares to be a disaster.

Moving Expenses

While some military members will still be able to deduct moving expenses, most people will no longer be able to do so.

Capital Gains on Home Sales

No major changes. Married couples can exclude up to $500,000 on a home sale so long as it was their primary residence for 2 or more of the past 5 years. Individuals can exclude up to $250,000.

Alimony

Divorcees who pay alimony will have to pay tax on the income, while those receiving the alimony will no longer be required to pay income taxes on the funds. This change will go into effect in 2019.

Cash Buyers Make a Comeback

The Impact of Private Equity Investors After the Crash

Before the housing bubble came into effect in the early 2000s the percent of cash buyers was closer to 20%. After home prices crashed cash during the Great Recession, cash buyers across the United States made up over 40% of home purchases in 2011 and 2012.

As property prices began to recover, private equity & hedge fund investors which purchased hundreds of thousands of homes across the country pulled back from the market & the volume of transactions driven by cash buyers declined.

In 2016 the US Treasury department started tracking all-cash buyers of high-end real estate in markets like New York and Miami.

Almost two-thirds of property purchases worth more than $2m in Manhattan and Miami were made in cash in 2015, according to research group RealtyTrac. More than half those purchases in Miami and almost a third of them in Manhattan involved limited liability companies used to shield the identity of buyers, according to RealtyTrac.

Outside of core hot markets cash purchases have been rather uncommon, until recently. Cash purchases are once again rising across the broader real estate market.

According to ATTOM Data Solutions 28.8% of US home purchases in 2017 have been cash purchases.

Five years after the housing market hit rock bottom, mortgage credit is finally returning to the healthy levels of the early 2000s, before the boom-bust cycle began. But all-cash deals remain well above normal levels, even as prices in many markets have pushed to record highs.

Many sellers prefer to work with cash buyers since the transaction is prompt and almost certain to go through. In some cases the cash buyer can also win with a lower bid as sellers value the certainty.

Cash rich foreign buyers & people who are either downsizing or moving from hot coastal areas inland also benefit from cash purchases as they save on loan origination fees and closing costs.

Proposed changes to the tax code which have passed both the House and Senate may accelerate internal migration away from the rich coastal states to lower tax flyover states, as state income tax payments will no longer be deductible from federal income taxes when the final bill is signed into law.

A Wall Street Journal article about the “cash buyer” phenomena highlights the trend is hitting markets that are not traditionally known as hot home markets. They mention Boise, Minneapolis & Raleigh as seeing a sharp uptick in cash buyers, with 42% of purchases in Raleigh being all cash purchases.

Where cash purchases dominate the local market, some buyers hoping for a quick flip might be buying unanticipated problems. On the above WSJ article a comment from Harvy Bogard stated the black tarry putty used by some builders stops working after 8 to 10 years, leading to foundation problems which would not occur if they used French drain systems:

It doesn’t surprise me that 42% of home sales in Raleigh, NC are now cash. Every other day I get a flyer in the mail, “We will buy your house now for cash.”

I believe a lot of the cash sales are driven by informed sellers unloading a house with foundation problems to uninformed speculative investors.

After looking in the crawl spaces of about 80 homes (for my third home purchase in Raleigh), I’ve concluded about 1/3 of the homes in Raleigh have foundation or moisture problems. The problems arise from our clay soil, combined with poor grading, water management, or location.

Some mortgage lenders and banks are trying to adjust to shifting consumer preferences toward cash purchases and faster real estate transactions.

- Better Mortgage Corp. is testing offering a loan which can be underwritten in a single day.

- Bank of America is offering new home owners a mortgage of up to 80% the property value after the home purchase is closed.

Recent Upgrades to Our Calculator

We recently made a number of upgrades to our homepage mortgage calculation tool.

Better JavaScript-Driven Charting Tools

For many years the chart on our site were powered by Flash. As popular as Flash once was, it caused many mobile browsers to crash. Steve Jobs shared his disdain for Flash in April of 2010.

Our initial solution to the support for Flash being limited to desktop devices was to not show charts to browsers which did not support Flash. We figured this to be a reasonable trade off because charts might take up too much space on smaller mobile devices.

In June Apple announced they would soon start blocking Flash on desktop devices as well.

Given how many home buyers use Apple devices we decided it made sense to upgrade our charts to shift away from Flash charts to JavaScript driven responsive charting. We found HighCharts to be the best solution for this implementation.

Here is what the old charts looked like

Now instead of there being 3 smaller graphs across the page, the remaining balance and annual payments are shown on a single wider graph & users can click the link below that to view a donut graph of payment breakdown by source. The top graph also contains tool tips so a user can see what portion of each year’s payments go to principal vs interest and so on.

Fewer Ads

Many publishers have responded to lower CPMs on mobile and the rise of ad blockers by adding more ad units, larger ad units & more invasive tracking to their pages.

Unblockable pop-ups, in-text ads, fly-in ads that move the text while you are trying to read it & auto-playing auto-generated video are just a few examples of the sort of stuff publishers are doing.

We have been approached by advertisers asking us to sell them a tracking pixel on the site…

I’m sure you’ve done this before, but I would specifically be asking to put a pixel on your website so that I could target your users other places on the internet outside of your website. I think the users of your site are similar to the users of my site, and the ability to target your users on other websites is something that I think could be valuable for my company.

Please know that I’m a serious ad buyer, and I spend 7 figures on advertising deals annually. If you would be open to me testing your users in this Retargeting trial, I would also be interested in buying ads directly on your site.

This test would be easy to set up, as I would just send a Google Retargeting Pixel to your webmaster who could implement it on the back-end. That’s it. I would then have the ability to target users of your website in other places and see if my ads resonate with them. I could be willing to pay you a monthly fee for this “pixel space.”

Thanks for your consideration!

…and we have universally refused these sorts of offers, as we view them as a violation of user trust. It is those sorts of backroom deals which have led to the rise of ad blockers.

We have taken a more sustainable user-friendly approach & reduced our ad load across the board. No page on our site has more than 2 ad units & the mobile version of our site only has a single ad unit.

Further, on the homepage and m. versions of our calculator users have the option of completely turning all ads off under the advanced settings menu which controls options like the display of amortization graphs.

Improvements to m. Version of Site

While both our regular homepage & the m. version of it use responsive web design features, on the m. version of the subdomain we also removed the ad unit which was near the calculation results so users can see the results faster on the small screen space mobile devices provide. We do not use any interstitial or anchor ads, to ensure the mobile experience is as fast and clean as possible.

We also disabled charts from appearing on the m. version, due to the constrained screen space, however a user can click the view desktop version of site to enable charting.

The m. version of the site still includes a mortgage rate table below the calculation results, so users can quickly see their current local market conditions, particularly in light of how BREXIT and other issues have rapidly moved US Treasury & mortgage rates.

Added Inputs for HOA & Home Insurance

Over the years we have had a number of requests to add the cost of insurance and HOA fees so buyers can see an “all-in” cost of ownership. We added these as input fields & made the calculation result output format more intuitive so people can quickly see their full monthly expenses while paying PMI & when PMI no longer required.

Perhaps the only major cost which our tool doesn’t currently account for is maintenance, but typically those expenses are lumpy and somewhat unpredictable. A good rule of thumb is 1% to 3% of the home purchase price, but this is a quite wide range & may be high for new homes while being low for older homes with major issues.

Further, mortgage interest deductions off income tax likely offset the maintenance costs for many home owners. There is always a trade off between the complexity of features in a tool & the usability of it. One way we offset some of these sorts of issues is for an input field like HOA we default it to zero & then on the results display we do not show HOA information if it is zero. Likewise if PMI payments are not required we do not show PMI info in the results.

Share This Calculation Result

Home purchases are typically the largest single investment most consumers make in their lifetime. Given this & the shift toward using mobile devices, we thought it made sense to make it easier for people to share calculation results.

On each calculation we create a short link which can be shared across the web or via mobile messaging applications.

This feature will help improve communications between partners (while someone is stuck at work, or such) & it will help agents sell more homes by making it easier for them to help their clients quickly see what is & is not affordable at a glance without any risks of miscommunications.

Features We Are Currently Thinking About

While we already have other calculators on our site which make it easy to compare the costs & benefits of refinancing, compare different loan term lengths side-by-side, print out an amortization table & help users see the impact of extra payments, we will soon modify the homepage of our site to make the CSS print feature easier to use to print out the amortization tables it creates. Updated: we now have the printer-friendly version of the homepage live, and users can share this version of their calculation with other people just like the short-URL version of the homepage.

We are evaluating adding other options, but want to be careful not to ruin the flow of the homepage calculator. We may also test surfacing some of the other calculation tools on the homepage in areas other than the sidewide navigation, but will be careful not to cloud the clean user experience of the homepage.

Thanks for reading this and using our website!

Have any feedback on features you would like to see? Please share your comments below.

Fannie/Freddie Raise Mortgage Fees

Beginning on April 1, Fannie Mae follow in Freddie Mac’s footsteps and formally raise the fees that they charge lenders, which will almost certainly pass these fees on to borrowers. The bottom line is that for virtually all borrowers, obtaining a mortgage is set to become significantly more expensive.

As mentioned earlier, Fannie/Freddie are currently hemorrhaging money at the combined rate of $1-2 Billion per month. While the government hasn’t yet determined how these two organizations – which currently underwrite 95% of all new mortgages and without whom, the mortgage financing system would collapse – in the mean time, it will certainly seek to limit their losses. Thus, the expansion of “loan-level price adjustments” should not have come as too much of a surprise.

Basically, Fannie/Freddie charge lenders fixed fees for all mortgages that they agree to purchase, and in return, the lender is alleviated of most of the risk. In the past, these fees were relatively modest, and certainly inadequate to offset the risk borne by Fannie/Freddie. Meanwhile, a few years have already passed since the collapse of the housing bubble touched off a wave of defaults, and since then, the mortgage behemoths claim to have learned a few lessons about the actual creditworthiness of borrowers.

Under the proposed changes, all borrowers will be charged an “adverse-market” fee of .25%, which can be paid upfront or rolled into the mortgage. Supplementary “risk-pricing” fees will be set in terms of the borrower’s credit rating, downpayment size, mortgage type, property type, and a handful of other factors. Only those borrowers (encompassing about 12% of the total) with FICO credit scores above 740, that make downpayments >25% for stand-alone residential properties will be exempt from this additional layer of fees. Everyone else will be required to pay up to 3% in fees, depending on their risk profile.

It’s worth pointing out that FHA loans are naturally exempt from these additional fees. In addition, “not all lenders sell all mortgages to the secondary market, so not all loans are subjected to the fees.” In addition, given that the profitability of issuing mortgages has surged in the last year (due to shrinking competition), it’s possible that some of the additional fees will be absorbed by lenders.

A few tips for borrowers, then. All else being equal, try to close on your mortgage before April 1. If you haven’t yet looked into the possibility of obtaining an FHA loan (which permit lower down-payments and lower credit scores), you should probably consider doing so. (However, FHA loans are also becoming more expensive and carrying higher restrictions). Next, make sure that your credit score is as high as possible, and that your credit report is free of errors. A difference of 5-10 points in your score could make a big difference in the fees that your lender charges you.

Finally, remember to shop around for a mortgage, and that all fees are ultimately negotiable. As I said, the dynamics of mortgage lending have changed dramatically since the collapse of the housing bubble, and it’s possible that your lender will agree to certain fee reductions in order to retain your business.

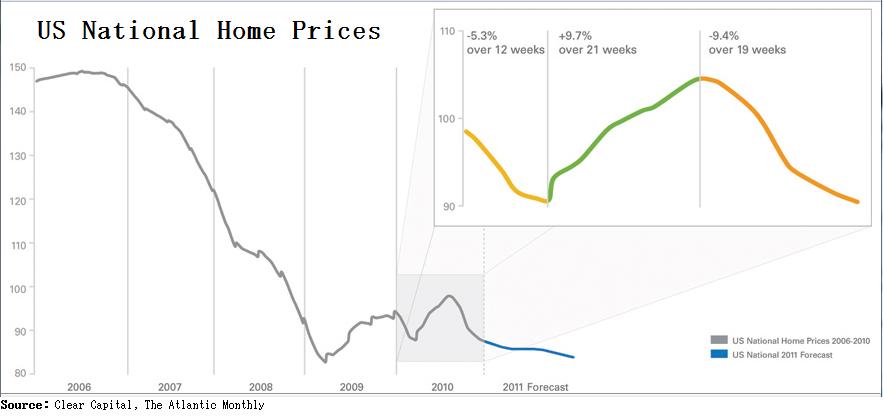

Housing Market: Double-Dip in 2011?

A few months have passed since I last offered an update on the state of the housing market. Since then, there have been a number of developments which suggest that 2011 could witness double-digit declines in housing prices, and that the long-awaited double-dip will finally materialize.

In an analysis of the housing market, it’s difficult to know where to begin. So much has been written on this topic over the last month and a trove of new data [Gary Shilling has dutifully compiled all of this data in a must-read research report] has been released, to the point that I experienced an acute case of information overload when researching this article. Here’s where we stand: the bellwether Case Shiller Housing Index “has risen 4.4 percent from its April 2009 bottom. But it remains 29.6 percent below its July 2006 peak.” According to some measures, this is already a larger decline than that which transpired during the Great Depression. While the national housing market stagnated in 2010, there was tremendous regional disparity. While prices fell ~20% in Dayton and Columbus, Ohio, they actually rose in 70% of major markets, including Washington DC (5%) and Honolulu (7.5%).

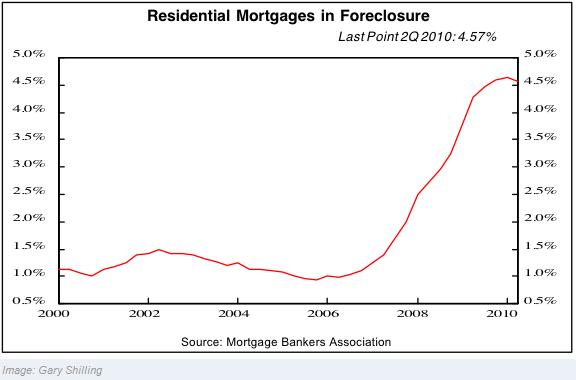

Meanwhile, the number of foreclosures also exploded: “Banks seized more than 1 million homes in 2010, according to RealtyTrac. That was up 14% from 2009 and the most since the company began reports in 2005….About 3 million homes have been repossessed since the housing boom ended in 2006…That number could balloon to about 6 million by 2013.” While the number of foreclosures fell in December because of legal uncertainty over the rights of lenders to repossess, delinquencies and defaults are still rising, and foreclosures will almost certain follow. 10% of all residential mortgages are now past due, and 4.5% are in foreclosure. (5 States: California, Arizona, Florida, Illinois and Michigan have accounted for more than half of the foreclosures). In addition, distressed properties accounted for about 30% of all home sales in 2010.

The clear consensus is that the only reason that the housing market didn’t completely collapse in 2010 is because the government intervened, in the form of a homebuyers tax credit. In hindsight, the tax credit merely pulled demand forward, instead of creating new demand. According to economist Nouriel Roubini, “If you look at the data, Case Shiller has been falling every month since the tax credit expired in May. Everyone who wanted to buy a home did so by April. That tax credit stole demand from the future…”

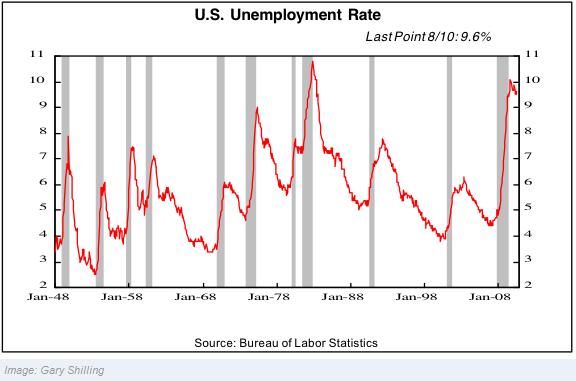

Going forward, there is more reason than not to believe that further declines are in store. There remains a massive shadow inventory of unsold foreclosed properties, which will expand further before it contracts. Mortgage rates have ticked higher in recent months from record lows, and besides, tighter underwriting standards are making it more difficult to obtain a mortgage. (Fannie Mae and Freddie Mac now underwrite almost 100% of residential mortgages). Meanwhile, the economy has only just escaped from recession, consumer confidence is low, and unemployment remains at a 30-year high of ~9.7%.

Even if you ignore the fundamental picture, econometric analysis suggests that housing prices have yet to “revert to the mean” of their long-term trend. Based on almost every measure, housing prices are still above historical levels, rent ratios remain high, and affordability indexes reflect inflated prices. From a purely financial perspective, then, housing prices would have to fall 20% in order to offset the appreciation of the bubble years. Moreover, it’s possible that the correction will “overshoot,” in which cases prices could drop by 25-30% before resuming their long-term average rise of 3.5% per year.

Yet, there are some economists who are cautiously optimistic. According to in Frank Nothaft, chief economist of Freddie Mac, “I do think we’ll see these housing prices bottom out, maybe by the spring.” Due to a drop-off in new housing developments, supply (not including the shadow inventory) is low. There is also hope that the economy will recover, and lift employment and consumer spending with it. As one columnist summarized, “The minute Americans see a real reason for hope…housing will come roaring back.” Even the most dire housing forecasts concede that some regional markets will probably rise in 2011.

From where I’m sitting, however, there really isn’t cause for much optimism. Unless you live in Hawaii or Texas, the next year (or two or three) will probably witness further declines.

Mortgage Lawsuits Spell Trouble for Lenders

A recent spate of lawsuits has accused mortgage lenders of impropriety or outright fraud at virtually every level of the mortgage process. Moreover, as lenders increasingly find themselves on the losing end, these lawsuits will have important implications for the future of mortgage lending.

Bank of America is currently in the process of resolving all of the disputes surrounding Countrywide Financial, which it acquired during the height of the housing boom. In 2009, it was sued by the state of Massachusetts for originating risky loans without verifying borrowers’ ability to repay the loans. BofA ultimately settled the case in May 2010, and agreed to “$18 million in loan modifications for Massachusetts homeowners, $3 billion in loan modifications for homeowners across the country, and a $4.1 million payment to the Commonwealth.”

However, the Attorneys General from the states of Nevada and Arizona have already filed suit alleging that BofA has failed to live up this agreement, as it “told consumers they would not be foreclosed on while requests for loan modifications were under way, not acting on the modifications within a specific time, making false promises to consumers and potentially selling their homes while they were waiting for decisions.”

Last week, Bank of America finally settled its case with Freddie Mac and Fannie Mae, in which it agreed to repurchase a substantial portion of Countryide mortgage securities, and subsequently write down $2-5 Billion of it. Meanwhile, All State Insurance, which also lost money on investments in mortgage securities, and MBIA, which lost money insuring such securities, have also filed lawsuits. Both allege that BofA deviated from its underwriting standards when it originated such loans. Such claims are supported by an internal Countrywide audit, which found that “approximately 40% of the Bank’s reduced documentation loans . . . could potentially have income overstated by more than 10% and a significant percent of those loans would have income overstated by 50% or more.”

Meanwhile, the State Supreme Court of Massachusetts “affirmed a lower court judge’s ruling invalidating two mortgage foreclosure sales because U.S. Bancorp and Wells Fargo did not prove that they owned the mortgages at the time of foreclosure.” While there was no doubt – as in thousands of other cases – that the borrowers were in default, the lenders failed to convincingly establish proof of ownership at the time of foreclosure. These cases were closely watched by foreclosure defense attorneys around the country, and it is likely that additional cases will now be brought forward.

The upshot is that lenders are finally being held accountable for lax origination/documentation practices that were begun during the housing boom. As if it wasn’t already clear, their operations will continue to be the subject of rigorous scrutiny, and it’s possible that more lawsuits will be brought forward.

Shop Around for a Mortgage

What a mundane and seemingly obvious piece of advice! And yet, according to the results of a recent survey by LendingTree.com, 40 percent of mortgage shoppers obtained just a single quote before settling on a mortgage. Given that the same poll established that 96% of consumers will comparison shop for most items, this is nothing short of astounding.

There are a few probable causes for this phenomenon. First of all, there is a small contingent of borrowers that either doesn’t understand that mortgage rates vary among lenders and/or mistakenly believe that rates are determined by the Federal Reserve Bank and that such variations are therefore trivial. Second, there is a factor of laziness. How else can you explain the 10% of borrowers that “admitted they had spent the same amount of time searching as it takes to brush their teeth.” There is also an aura of complexity surrounding mortgages, which spurs fatigued borrowers to simply choose any lender at arm’s reach. Finally, there is a misconception that lending standards have become so stringent that borrowers should immediately pounce on the first approval that they receive.

While mortgages have become a commodity product over the last decade, there is still a tremendous amount of variability between mortgage lenders, in terms of rates, points, fees, service, and lending standards. At the very least, it’s worth speaking to a few different lenders to make sure that you receive a good deal, fair terms, and good service.

The first step is to use the newspaper, internet, friend’s referrals, etc, to develop a preliminary list of 3-5 potential lenders. (You may also want to consider including a mortgage broker on the list. While this will add an extra layer of fees, a good broker will do your mortgage shopping for you and might even be able to help you save money overall). The next step is to contact each lender and ask them basic information about the types of mortgages that they offer and are potentially suitable for you. While you should focus on the financial (i.e. rates, points, fees) parameters, you should also inquire about other points of distinction. (The FTC has created an excellent table that you can use to comparison shop).

In order to give you an accurate quote, each lender will probably ask you for personal financial information. Bear in mind, however, that in order for them to offer you a precise estimate, they will need to separately pull your credit history, which could adversely affect your credit score. For that reason, it’s probably only worth obtaining a Good Faith Estimate only once you have settled on a property, and/or you know approximately how much you will need to borrow. If you elect to obtain pre-approval prior to shopping for a home, remember that you are not bound to that lender. You can always continue mortgage shopping or start afresh, after identifying the home that you wish to purchase.

Remember that different lenders have different lending standards. Don’t be discouraged if you are rejected by the first lender(s) that you contact. Conversely, don’t automatically accept the first offer that you receive. Even if you have a mediocre credit score, you might still be able to find a handful of lenders that are willing to give you a mortgage at an attractive rate.

Finally, there is something to be said for dealing with a broker/lender that you trust. As the LendingTree survey confirmed, shopping for a mortgage is a daunting process. It might ultimately be worth paying .05% more if you feel more comfortable with one lender than another.

Appraisals Continue to Affect Closings

As if obtaining a mortgage loan wasn’t difficult enough, it turns out there was one more obstacle which has to be overcome: the appraisal. Thanks to new federal regulations, appraisals have now become a nail-biting experience. The best advice for both buyers and sellers is to avoid obtaining one altogether.

Unfortunately, all lenders will stipulate that an appraisal must be performed in order for the mortgage to be originated. During the inflation of the housing bubble, this was hardly an onerous requirement. Given that appraisal is inherently more art than science, it was easy enough for appraisers to adjust their comparison tables and deliver a value that was in line with what the buyer and seller had agreed upon. In fact, many appraisers reported receiving pressure from lenders to deliver a value (so that the sale would close), thereby minimizing the importance of their role in the process.

In some ways, this changed as a result of the Dodd-Frank financial reform bill and the related Home Valuation Code of Conduct (HVCC). Among other things, the independence of appraisers (such that they would be immune from third party pressure) was stipulated. This led to the creation of Appraisal Management Companies (AMCs), which has unfortunately led to a decrease in quality: “They mostly care about getting the appraisal done quickly and cheaply, not necessarily well. And they take a good chunk of the appraiser’s fee—often more than half—with the result that appraisers say they can no longer make a living; competent people are fleeing the profession.”

Moreover, appraisers still report being pressured from lenders – this time to deliver lower appraisals – “from lenders who want to make sure they have enough equity to cover them even if home prices fall further. As if this were not enough, a preponderance of short sales and foreclosures in some areas is making it difficult for appraisers to find comparable properties, and is putting downward pressure on both home values and appraisals. The news has been filled with horror stories of second and third appraisals that came in 10% (or more lower) than the first appraisal, making it difficult to complete the sale. According to the National Association of Realtors, “One in 10 member agents said they’d had a contract canceled as a result of a low appraisal, 13 percent said they’d had a contract delayed, and 16 percent said they’d had a contract negotiated to a lower sales price as a result of a low appraisal.”

In short, it’s probably best to avoid having an appraisal performed if you can help it. If the buyer and seller can agree on a price, it’s pointless to request the opinion of an appraisers unless it is ordered by the lender as a precondition to mortgage financing. If, on the other hand, you are stuck with an unpalatable appraisal, you should challenge the valuation and/or request a home inspection. If the appraiser isn’t willing to bend, you might be forced to find another appraiser.

Mortgage Pre-Approval is Still Worth Getting

The majority of home-buyers conduct their house-shopping before obtaining financing. After all, how can you obtain a loan for a property that you have not yet purchased?! What if I told you, however, that you could achieve a loan guarantee from a prospective lender at the beginning of the process, such that you could close on the purchase of a home immediately after selecting it?

Known as pre-approval, this guarantee represents a commitment by a specific lender to underwrite a mortgage for the potential purchase of a home. Based essentially on your credit score and a handful of other selected financial characteristics (pertaining to your assets and income), the lender will determine the maximum monthly payment you can afford to make. Prevailing interest rates are then applied to this figure in order to determine the maximum overall mortgage amount.

The advantages of pre-approval are two-fold. First of all, you can shop for a home with the confidence that you can obtain financing for it as long as it falls within the financial specifications laid out by the lender. Second, the pre-approval letter can be used as a bargaining chip in negotiations with the seller. For example, if two potential buyers make similar offers for the same property, the seller might be more willing to accept the offer from the pre-approved buyer, because it is more likely that the sale will close quickly. The advantage to the lender is that the borrower is more likely to return to it when he begins the actual process of obtaining a mortgage.

Unfortunately, it seems that lenders are now reluctant to grant pre-approvals, as part of a general trend towards stricter lending standards: “The rules from the Department of Housing and Urban Development require lenders to issue a binding good-faith estimate of total closing costs within three days of submission of a formal loan application.” In other words, it is not so much the pre-approval itself that frightens lenders, but rather locking in the closing costs.

Instead, lenders are turning to pre-qualification, which is “a less rigorous assessment of how much they can afford to borrow based on unverified financial data.” In such cases, a pre-approval might only be granted after the borrower’s loan application has been formally reviewed. While a pre-qualification is useful in that it gives the borrower a reasonable idea of the maximum loan they can hope to obtain, it is ultimately non-binding and thus, unreliable. Even if it is based on the same underwriting standards, the fact that it is only a pre-qualification means that a lender is not legally bound to it in the same way it would be to a pre-approval.

Borrowers should ultimately be aware of this distinction and push for a pre-approval. Most lenders should theoretically still be willing to issue them; it might just be a matter of persistence and understanding the process for applying for them.