Homebuyer Tax Credit Could Expand

The federal government’s homebuyer tax credit has been a boon for both the housing industry and the housing market, causing a surge in sales over the last few months. In fact, the program has been such a success, that some states are now introducing their own versions, and stakeholders are lobbying both to expand the federal program and to extend its deadline.

In its current form, the “tax credit is equal to 10 percent of the home’s price, up to $8,000. So, for example, if a buyer is paying $50,000 for a house, the credit would be worth $5,000. The tax credit never has to be repaid. Last year, Congress created a different tax credit, but that one was effectively an interest-free loan. This money involves no repayment or interest…Buyers will get the money when they claim the tax credit while filing their federal income taxes for 2009.” If a taxpayer owes less than the tax credit he is due, then he is still entitled to receive the difference.

Given that the program is slated to expire on November 30, several lawmakers have already moved to legislate an extension. In fact, there are two bills currently winding their respective ways through Congress: “H.R. 101, The Economic Recovery Through Responsible Homeownership Act of 2009, which would provide up to $10,000 in tax breaks to any homebuyer who makes a qualifying down payment and H.R. 1245, the Homebuyer Tax Credit Act of 2009, which would provide a tax credit of up to $15,000.” The Senate is currently working on developing similar legislation.

Another change could affect borrower eligibility. With the current credit, “Congress set an income limit for the full credit. For a single person, it’s $75,000 and for married couples, it’s double that.” With the extension, it’s possible that these income limitations (and maybe even the requirement that the credit be applied towards a first-time home purchase) could be eliminated, in order to make the credit available to more people.

Meanwhile, the federal government is not the only one working overtime on this issue. New York recently became the first state (that I know of) to implement a similiar program, which “would allow home buyers to take a dollar-for-dollar deduction of 20 percent of mortgage interest paid, Gov. David A. Patterson and other state officials announced. The remaining 80 percent of the mortgage interest paid for the year will be treated as usual, as itemized tax deductions.” For some borrowers, this could amount to savings in excess of $1,000 a year. Not a bad deal, especially when you factor in the federal money. It will be interesting to see if other states follow suit, and we’ll keep you posted as this story unfolds.

Retirement and Mortgages

Convention wisdom has always held that its best to enter into retirement without any outstanding debt, especially not a mortgage. That wisdom has been turned on its head as a result of the financial crisis, which devastated the savings of those approaching, or already in retirement. “Now, many people retire while still paying that monthly home-loan bill,” reports one source.

Despite the crisis, however, it turns out that common sense still applies: “It’s better to pay down your mortgage than to carry it into retirement. Or at least it is if you have the money set aside in a taxable or tax-deferred account.” This true for a couple of reasons. First, the return that you can expect to earn on your (retirement) savings is probably well below your mortgage rate, which implies that you are actually losing money by not repaying your mortgage. As a general rule of thumb, it’s always better to pay down your debt, so that you know exactly where you stand in your personal financial situation.

If you can’t afford to repay your mortgage before retiring, there is another option: a reverse mortgage. While there are several variations, reverse mortgages essentially enable you to draw-down the equity in your house, eventually freezing it at a certain level. Unlike with a conventional mortgage, however, there is virtually no risk of foreclosure. “Reverse mortgages have traditionally been chosen by older Americans who can’t cover everyday living expenses or who otherwise need cash for such things as long-term care premiums, home healthcare services or home improvements.”

Of course, there are drawbacks. Namely, the costs can be significant and the mortgages are often deliberately complicated. “Borrowers should consider discussing the appropriateness of a reverse mortgage given their current financial situation and the other options available to them before applying for a reverse mortgage.” There is also the risk that receiving payments in connection with a reverse mortgage could render you ineligible for certain federal retirement programs.

But the benefits are just as manifold: “You can take your payment as a lump sum, a monthly cash payout, a line of credit held in reserve or a combination of all three. No repayment is due until the last homeowner moves out or dies, at which point the home can be sold to pay off the debt. The loan repayment can never exceed the home’s market value (even if it declines), absolving your heirs of any liability.” Portability means that you can take your reverse mortgage with you if you decide to move. Most importantly, you can use it to pay off your current mortgage, and move into retirement debt-free!

Underwater Mortgages Increase, but No Break for Borrowers

According to a new report by Deutsche Bank, and investment firm, the number of borrowers with underwater mortgages – those who owe more on their mortgage than their homes are worth – is projected to skyrocket in the next few years. This proportion, “will nearly double to 48 percent in 2011 from 26 percent at the end of March, portending another blow to the housing market.”

Deutsche Bank didn’t offer much in the way of context/analysis for its figures, which is somewhat surprising since several indicators of the housing market have begun to tick up. Regardless, the projections are eye-opening, to say the least. Everyone already knows about the problems affecting the riskiest class of mortgages. With regard to subprime loans, “69 percent will be underwater in 2011, up from 50 percent in March, Deutsche said. Of option adjustable-rate mortgages — which cut payments by allowing principal balances to rise — 89 percent will be underwater in 2011, up from 77 percent.”

Those following the housing market probably would have also anticipated that some of the most distressed regional markets would see a rising percentage of underwater mortgages, many of which were no doubt funded using the risky mortgages cited above. For example, “Las Vegas and parts of Florida and California will see 90 percent or more of their loans underwater by 2011.”

Few, however, would have expected such dire predictions for prime loans, which “make up two-thirds of mortgages, and are typically less risky because of stringent requirements.” As a result of a projected 14% price decline up to 41% of prime conforming loans may be characterized by negative equity by 2011. “Forty-six percent of prime jumbo loans will be larger than their properties’ value, up from 29 percent, it said.”

Most troubling, perhaps, is the notion that such borrowers won’t receive a break from lenders, nor from the government. Currently, the practice of reducing one’s mortgage (known as a cram-down) as a result of personal bankruptcy, remains taboo as a result of industry pressure. “House Financial Services Committee chairman Barney Frank (D-Mass.) has already warned that if more loans aren’t worked out, he’ll renew the push to allow bankruptcy judges to order reductions in mortgage amounts.”

In fact, government legislation appears to be moving in the opposite direction. Arizona, for example, is contemplating changing its laws on deficiency judgements, which currently serve to prevent a lender that “forecloses on a home mortgage to recover the balance of what is owed the lender if the foreclosure sale doesn’t produce the full amount…The changes, which haven’t yet taken effect, impose new eligibility requirements to qualify for protection against a deficiency judgment. One is that the borrower must have lived in the property for six consecutive months.” If this takes effect, then borrowers that walk away from their underwater mortgages might see the balance stay with them forever. What’s next – a return to the days of debtor prisons?

Housing Data Paints Conflicting Picture

Mortgage rates have remained relatively stable. How has this trickled down into the housing market? In a nutshell, housing prices are stabilizing, but it’s unclear whether the market has yet to bottom. In addition, national averages mask regional differences, and soft spots remain in certain markets, and in high-end housing.

Let’s zoom in on some specific data points: “The Standard & Poor’s/Case-Shiller price index, a closely watched gauge, showed that single-family-home prices rose 0.5 percent from April to May, the first monthly increase since 2006…The federal government reported an 11 percent rise in new-home sales from May to June, the largest monthly gain in nine years. Sales of previously owned homes jumped for the third straight month, up 3.6 percent in June.” Meanwhile, “The median sales price was $206,200, down from $234,300 a year and $219,000 from May.”

At face value, these statistics seem to portray a market that has entered the recovery stage, but they should be interpreted in context. First of all, “Home sales quite often jump in June, the height of the spring selling season.” This June was particularly bountiful because of the federal government, which is offering an $8,000 tax credit for first time buyers, and implemented a de facto moratorium on foreclosures.

However, given the seasonality of the housing market and the fact that both of these government programs are slated to expire soon, “It makes more sense to compare them [home sales] with the same month a year ago. That comparison is less kind — sales were down 21.3% from June of 2008. Seasonally unadjusted data show a total of 36,000 new homes were sold last month, the lowest June total since 1982.” It should also be pointed out that the data is derived from a survey – rather than from actual numbers- and carries a margin of error, such that the true figure could very well be negative.

There are also significant regional disparities contained in these numbers. “Sales were strongest in the Midwest, where they jumped 43 percent from May’s total. Sales climbed 29 percent in the Northeast and 23 percent in the West. They declined slightly in the South.” In California, Florida, Nevada, and Arizona, prices continue to fall, and foreclosure rates are rising.

The high-end market, meanwhile, continues to tank, due mainly to a delayed bursting of the bubble and changes in lending standards. “The supply of unsold homes priced above $750,000 swelled to around 17 months in June, up from a 14.5-month backlog one year ago. A recent forecast by analysts at J.P. Morgan Chase & Co. said it would take until at least 2012 for the expensive-home market to recover and that peak-to-trough declines could surpass 60%, compared to 40% for the rest of the market.”

It’s quite obvious that from an historical standpoint, then, the housing market remains quite depressed. But what about the future? “ ‘The freefall is over,’ says Dean Baker of the Center for Economic and Policy Research.” Warren Buffet agrees: “Most of the problems in the housing market will be over in 18 months or something like that.” Alan Greenspan, however, thinks that “Home prices had stabilized only temporarily. ‘It is possible that could get a second wave down.’ ” Other analysts point out that for as long as the overall economy – specifically the employment situation – remains weak, the housing market will fail to recover. In addition, should interest rates rise suddenly and/or another wave of foreclosed properties hit the market, the market could certainly trend downward.

“Strategic Default” on the Rise

According to a recent headline-grabbing study, “26% of the record numbers of home mortgage defaults across the country are ‘strategic‘ — that is, calculated economic decisions to bail out of loans by owners who actually have the money to make the payments but can’t handle the negative equity they’re carrying caused by local property value declines.” In most of the coverage to-date surrounding the foreclosure crisis, this class of defaulters has been largely ignored.

The study found that there were a few variable which correlate closely with borrowers’ respective willingness to intentionally default. First, and most obviously, is the value of the mortgage compared to the current value of the home. Specifically, those whose mortgages are most “underwater” are also most willing to default: “Researchers found that almost no homeowners would default if their equity shortfall was less than 10% of their home’s value, but one-in-six homeowners would default if their equity shortfall reached 50% of their home’s value.”

In controlling for age, location, and education level, the study determined that “Well-educated borrowers, homeowners in the Northeast and West, and people under 35 or over 65 were less likely to have moral reservations about choosing to walk away from making mortgage payments.” One’s sense of morality evidently plays a strong role in this calculation, with those who regarded strategic default is immoral 2-3 times less likely to default than their amoral counterparts. This relationship, however, is also proportionate to the size of one’s negative equity position: “While four out of five homeowners said they believed it was morally wrong to intentionally default, as negative equity rises, more borrowers—including those who said strategic defaults were immoral—would consider walking away.”

However, morality (in the case of strategic default at least) is apparently received from social cues. In other words, borrowers surrounded by default were themselves more likely to accept default as an amoral possibility. “The higher the number of foreclosures in a given ZIP Code, the higher owners’ willingness to walk away, the researchers found, suggesting what they call a ‘contagion effect that reduces the social stigma associated with default as defaults become more common.’ ”

This has some important implications for the recent federal legislation, which has aimed to prevent foreclosure by simply helping borrowers to modify their monthly payments, thereby making their mortgages more affordable. However, this legislation is built implicitly on the ideas that underwater borrowers will still repay their mortgages, and that affordability should be measured/enhanced on a monthly – rather than an aggregate – basis. If this report is to be believed, both of these assumptions are questionable. Perhaps this means that we will soon seen a corollary to this legislation passed, in which borrower equity (i.e. mortgage value) is also adjusted. Or maybe not.

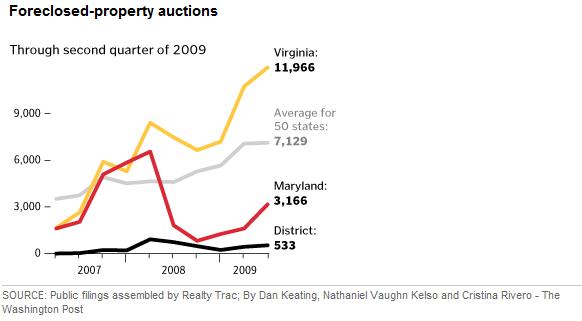

Distressed Housing Attracts Speculators

There seems to be an important exception to that notion that this is a buyers’ market when it comes to housing: distressed real estate. Properties that are delinquent and nearing foreclosures or are already in foreclosure are now attracting bubble-like interest.

According to a report by RealtyTrac, “1.5 million U.S. owners have been told they are in danger of losing their homes. The company Thursday said one in every 84 households got at least one foreclosure notice during the first six months of the year, a new record.” As a result, “The existing home market is still vastly oversupplied, and we continue to be inundated with an influx of distressed and foreclosed properties,” observes another analyst.

Unfortunately – at least from the standpoint of “genuine” buyers – many of these properties are being snatched up by speculators and institutional investors, who have finally found a corner of the real estate market that remains buoyant. “Vornado Realty Trust, one of the biggest real-estate investment trusts in the U.S.,” made headlines when it announced its intention to “raise $1 billion for a private-equity fund to invest in the wave of distressed properties expected to hit in the next few years.” According to marketing materials, the fund is aiming for a 20% annualized return on its investment, which is in indication of just how excited people are about the market for foreclosed properties. Distressed commercial real estate, meanwhile, is nearing $100 Billion and growing rapidly.

Other investors, meanwhile, are hoping to benefit indirectly from a new federal program “designed to stabilize and revitalize neighborhoods ravaged by foreclosures and abandonment.” Across the country, “Out-of-state speculators continue to swoop into these neighborhoods, plucking properties they might fix up and rent out. Then again, they might try to flip them or simply sit on them, perhaps fouling any attempt to stabilize these areas.” These properties are being snatched up for eye-poppingly low prices- under $10,000.

Real estate agents are also getting into the game. A just-announced arrangement “will give local RE/MAX agents…access to RealtyTrac’s database of properties that are in some state of foreclosure — including properties in default, homes scheduled for public foreclosure auction and bank-owned properties…Going forward, prospective homebuyers visiting remax.com also will be able to search RealtyTrac’s database.” While ostensibly affording both buyers and sellers of foreclosed homes more opportunities, a byproduct of this arrangement is that speculators will also have an easier time spotting such properties.

Investors have another advantage – beside deep pockets – over regular homeowners; they almost always pay cash. Until the credit crisis is fully resolved and banks once again trust each others’ credit, it seems speculators will have the upper hand.

Foreclosures: No End in Sight

The recent stabilization of the housing market now appears to be a mirage, brought on by stopgap measures. “Until recently, many banks have put off launching foreclosure action on the troubled properties, in part because they had signed up for the Obama administration’s home-stability plan, which required them to consider the alternative of modifying loans to make it easier for borrowers to make payment. Unfortunately, the federal push to promote loan modifications and the related moratoriums that some states have imposed on foreclosures are already fading, at which point the foreclosure crisis is likely to expand.

“A new set of economic theorizing holds that any bottom that might have been glimpsed was a false one – just a plateau before a bigger drop, when lenders try to clear their books of bad loans. If that’s the case, the economic hole starts to look a lot deeper, and the housing crunch becomes another part of a larger, vicious cycle.” In other words, if banks move to place a fresh supply of foreclosed properties on the market, it will cause all prices to suffer. This will put even more pressure on those whose mortgages are already underwater (1 in 5, according to one estimate), and perhaps compel banks to race even faster to liquidate mortgages in default.

According to RealtyTrac, April “was the worst month ever, with more than 340,000 properties in some state of foreclosure nationally…They are expecting June’s numbers (to be released next week) to ‘give April a run for its money’ as worst month ever.” This was discerned from a large uptick in delinquent mortgages, many of which can be expect to result in foreclosures. “In the first quarter, some 1.8 million homeowners nationwide fell behind on their loans by 60 to 90 days, a 15% increase from the prior quarter, according to Moody’s Economy.com. The research firm said that loan defaults rose sharply as well, to 844,000 in the first three months of this year.”

Who’s to blame for this? The government appears to be doing as much as it can. “Foreclosure counseling is an extremely effective service; HUD reports that 45 percent of those who participated in 2008 were able to hang onto their homes.” While estimates vary, hundreds of thousands of borrowers have probably benefited from the loan modification program.

The problem is the banks, which continue to prefer foreclosure over loan modification. According to a new Federal Reserve paper, “lenders rarely renegotiate. Fewer than 3 percent of the seriously delinquent borrowers in our sample received a concessionary modification in the year following the first serious delinquency.” There are two main reasons for banks’ entrenched resistance: “The first is ‘self-cure risk,’ which refers to the situation in which a lender renegotiates with a delinquent borrower who does not need assistance…The second cost comes from borrowers who default again after receiving a loan modification. We refer to this group as ‘redefaulters,’ and our results show that a large fraction (between 30 and 45 percent) of borrowers who receive modifications, end up back in serious delinquency within six months.”

More on loan modification- and why it’s failing – tomorrow….

Plain-Vanilla Mortgages as a Solution to Mortgage Crisis

One of the cornerstones of the Obama administration’s plan to overhaul the US mortgage system is an emphasis on so-called “plain-vanilla” financing. Specifically, “The government would give its seal of approval to a handful of mortgage types — a standard 30-year fixed-rate mortgage and perhaps a few varieties of adjustable-rate loans. For a loan to get the ‘vanilla’ label, the lender would have to verify borrowers’ income and have them set aside money for property tax and insurance.” A 20% down-payment would be required, prepayment penalties would be eliminated, and all fees/costs would have to be clearly stated. [See chart below, courtesy of WSJ].

The primary purpose of the plain-vanilla system would be to protect borrowers, many of whom were burned by complicated mortgages during the height of the housing boom. Types of mortgages have exploded both in number and complexity, such that there are now hundreds of different variations, requiring various levels of risk disclosure and creditworthiness. Ostensibly, this innovation was designed to help consumers by giving them more choices. Human nature being what it is, many borrowers opted for the riskiest mortgages. Meanwhile, banking profits soared. Given how opposed the banks are to the return to plain-vanilla lending practices, it’s pretty obvious as to who is benefiting most from the current system.

There is a strong political bend to this regulation, given the assumptions about human nature that it makes. Still, there is something to be said for simplicity. A fixed-rate mortgage is predictable and easy to understand. Income verification confirms the borrower’s ability to afford the mortgage, and a large down-payment lowers the possibility of default. Sure there are borrowers who liked the freedom to use their mortgage to make a bet on the direction of interest rates, and/or who successfully exploited liar’s loans to purchase a house they otherwise wouldn’t have received lending approval for. But for everyone who came out ahead with a zero down payment ARM, anecdotal evidence suggests that there are 9 who came out behind and are now in default.

Under the new system, those who want to play roulette with their home/finances can still do so, but will be strongly discouraged in the form of un-preferential treatment/pricing. “According to the administration’s ‘white paper’ on the proposal, the agency ‘could impose a strong warning label on all alternative products; require providers to have applicants fill out financial experience questionnaires; or require providers to obtain the applicant’s written ‘opt-in’ to such products.’ ” In this way, banks will also be protected, since consumers can no longer pretend that they weren’t aware of the risks when they signed up for the mortgage.

In the wake of the housing crisis, risk aversion has increased, and it looks like banks/consumers are actually one step ahead of the government. “With the housing bubble burst and mortgage rates near historic lows, fixed-rate loans — 30-year, 15-year and other types — now account for about 95 percent of the market,” compared to only 50% during the height of the boom in 2004. But people have short memories. If this regulation passes, it will make it more difficult for people to overextend themselves when the economy begins to recover.

The Government Wants to Help you with Your Mortgage

Barack Obama and the rest of the federal government continues to roll out new initiatives designed proximally to help mortgagers in need, and ultimately to stimulate the ailing economy. At this point, pretty much everyone is eligible for help, regardless of what stage of the process they are at.

For those that already have a mortgage and are facing foreclosure, the government has pledged money to incentivize banks to grant loan modifications for qualifying mortgagers. “To be eligible, a homeowner must have a monthly mortgage payment larger than 31 percent of their gross income. The monthly payments of those who qualify are lowered to the 31 percent limit. Lenders can do this by reducing interest rates to as low as 2 percent, by extending the term of the loan to 40 years or by deferring principal.” Borrowers are then placed in a temporary program whereby they must make their reduced payments successfully for three months, after which points they see their loans permanently modified.

On the one hand, the Treasury Department is trying to make it easy for eligible borrowers to receive modifications: “About 100,000 homeowners across the country so far have been extended loan modification offers. ‘We are encouraging servicers to staff up, establishing a hotline for homeowners, looking for new tools to expedite this process, working with communities to get the word out about resources available to homeowners,’ ” declared the department’s spokesperson.

At the same time, those who have applied tell stories of long waits, lots of uncertainty, and probable rejection. There are two related reasons for this discrepancy. First, there is a lack of lender impetus to facilitate loan modifications: “Housing counselors say that while 15 lenders — including major ones like Bank of America, CitiMortgage, Chase and Wells Fargo & Co. are participating, many have yet to fully train people to process the applications. As a result, housing counselors say they often receive mixed signals, with different lenders offering different interpretations of the guidelines.”

Second, the mortgageholders (i.e. investors) have the ultimate say in whether a mortgage can be modified. In situations where the value of the mortgage exceeds the value of the home, investors are more willing to agree to modification, because a foreclosure would result in lower remuneration. In relatively healthy markets, however, investors are more reluctant, especially since all of the incentives are directed towards the banks.

Ultimately, “One thing is clear: Homeowners who have a HUD-approved housing counselor championing their cause are more likely to get a modification than those who try it on their own. Housing counselors say they often understand the program’s guidelines better than the people answering phones for lenders, so they know how to pursue a case aggressively.”

Stay tuned for tomorrow’s post, where I will outline the homebuyer tax credits and the implications of the proposed Consumer Financial Protection Agency…

Are Falling Home Prices a Symptom of Low Appraisals?

Along with predatory lenders, ignorant homebuyers, and greedy investors, overly optimistic appraisers have been one of the main targets of those looking to mete out blame for (the collapse of) the housing bubble. Specifically, appraisers have been criticized for their lofty valuations, which may have contributed to “excessive” house price inflation. Appraisers counter that they were only doing their job, and that the real blame lies with the lenders that pressured them into simply confirming sale prices in order to make sure that deals closed.

Now, however, the pendulum may have swung too far in the opposite direction, such that appraisers have suddenly become overly conservative. Again, the appraisers blame the lenders, who this time around are driving appraisal valuations down in order to make sure that they don’t lend more than the home is actually work. “In some cases, lenders are requiring that appraisals be based on sales closed within the past three months rather than the prior six-month norm, appraisers said. Some lenders are also asking for comparisons with at least one sale in the past 30 days.” Also faulted is the new mortgage appraisal system, whereby home valuations are performed by appraisal management companies. While the change was supposed to prevent banks from directly pressuring appraisers by placing a buffer between them, the actual result was to commoditize the appraisal and drive down quality.

A similar trend can be seen in the rise of Broker price opinions, or BPOs, which “are performed by real estate agents who, unlike licensed appraisers, have no regulatory oversight of their valuations. BPOs are attractive for lenders because they cost between $40 and $65, compared with about $350 for an appraisal.” Meanwhile, since the agents have also been engaged to sell the property, they are incentivized to keep prices low, in order to maximize the chances of a sale. [It should come as no surprise that BPOs are illegal in 23 states].

The result is that appraisals are still leading the market, only this time around they are tugging prices downward instead of dragging them upward. Naturally, homeowners are furious. “When the homes are then sold at ‘fire-sale prices,’ the rest of the neighborhood suffers, especially in areas with clusters of distressed sales,” which is causing prices to fall across the board. Some home-sellers are being forced to drop their prices at the last minute in order to hold onto buyers with appraisal contingencies built into their mortgage contracts.

Homebuilders are also suffering since banks will no longer approve mortgages for properties that are determined to be overvalued, with the result that some new homes are being sold below cost. Meanwhile, those looking to refinance or take out home equity lines of credit are facing an uphill battle. Appraisals are coming in so low that creditworthy borrowers are being rejected outright for refi’s and/or watching the bank freeze their LOCs.

The keys to making sure that you get an appraisal that you’re happy with is to understand how the appraisal process works and then to double check the final report for errors. Most appraisals use a weighted average of the estimates from a sales comparison approach, income approach, and cost approach. Begin by making sure that comparative sales are actually comparable, and that there are not a couple of questionable homes dragging down the average. From a cost perspective, make sure that the appraiser took accurate stock of your home. For example, did he factor in all of the rooms and all of the renovation work you have completed recently?

In the end, unfortunately, appraisal is more of an art than a science. In other words, prices are constantly fluctuating and your home’s “true” value might be different yesterday from tomorrow. Really, a home, like anything else, is only “worth” what somebody else is willing to pay for it.