Is the Housing Market Stabilizing?

This last week saw a flurry of data, painting a predictably contradictory picture of the housing market. The debate over whether housing prices have stabilized now looks something like this: “House Prices Have Bottomed;” “No They Haven’t;” “Yes They Have;” “Not Yet!” That’s not to say that the conclusion is that in fact housing prices have not yet bottomed, but instead that “evidence” can be found to support either conclusion and also that there is unreported data muddying the picture.

On the plus side, pending home sales rose 6.7% nationally in April, and even faster in some regional markets. Previously owned U.S. homes rose by 2.9% over the same period. Meanwhile, “Existing-home inventories are down to 9.8 months’ supply, higher than their long-term average of six months, but off their recent peak of 11.3 months.” [See chart below courtesy of WSJ] In other words, almost all of the data points appear to be either improving, or at least slowing in their rate of decline…..that is, until you look at what’s not being directly captured by the numbers.

First of all, the data itself is prone to manipulation, since much of it is self-reported, rather than compiled in accordance with some kind of universally-accepted standard. For example, pending home sales are being booked earlier and earlier, such that a smaller percentage are ending in actual sales. “A 33-percent jump in pending sales from February to March, for instance, did not bring a corresponding increase in closings a month later. In fact, April closings were up less than 4 percent from March.” As a result, “closed sales went from 89 percent of the previous month’s pending sales in June to 80 percent in July and have ranged from 60 percent to 84 percent since.”

Then there is the inventory data, which by its very nature doesn’t reflect homes whose owners would like to sell, but haven’t yet been listed. “There is a massive shadow inventory of bank- and investor-owned homes, enough to push existing-home supply to 12 months, notes one economist.

Ultimately, a full housing recovery is unlikely for as long as house prices remain depressed. The data and analysis surrounding this question is perhaps the most nuanced.

On the one hand, “The Federal Housing Finance Agency’s quarterly purchase-only house price index shows nationwide home prices fell 0.5 percent from the fourth quarter 2008 to the first quarter 2009,” compared to a decline of 3.3 percent in the previous quarter. An analysis of San Diego, where the housing market collapse was especially sever, indicated that prices are now well below their long-term average.

On the other hand, “Healthier regions, including ‘many parts of the Northeast, have only just begun to suffer price declines…Together, these factors could drag on prices through much of 2010, pushing the Case-Shiller index to a total decline of 40%.’ ” (It has already declined by 27%). Banks are certainly conscious of this possibility and are taking longer to approve mortgages. Given that interest rates are now rising and mortgage applications are leveling off, it could be a while longer before the market really stabilizes.

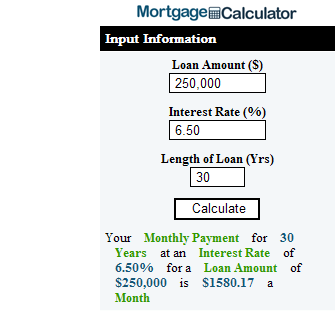

WP-Mortgage Calculator Widget / Plug in for WordPress

We recently created a free Mortgage Calculator plugin that you can easily install in any WordPress blog in under 5 minutes!

How it works:

Hit the calculate button and see the results in real-time on your site. This helps you keep your site visitors focused on your site and your inventory – instead of sending them elsewhere.

If you look at the left sidebar of this blog you can see it in action, and here is an image of the calculator in use

Download WP-MortgageCalculator Now:

You can download WP-Mortgage Calculator here now! 🙂

Installation instruction for WP-MortgageCalculator:

This free calculator installs in the sidebar of your WordPress blog as a widget. The calculated results appear directly on your website, so you keep your readers engaged and active on your website!

——————————————————

Step 1: Unzip the WP-Mortgage Calculator package and

put in it in your plugins folder located at

wp-content -> plugins

——————————————————

Step 2: after unzipping the files upload them to your remote server using an FTP program.

The (4) files included in this package are

mc_calculate.php

mc_linktext.php

mortgage-calculator-logo.gif

mortgagecalculator.php

——————————————————

Step 3: log in to your WP admin panel, located at

/wp-admin/

Click the plugins link, which will send you to

/wp-admin/plugins.php

and enable the Mortgage Calculator Widget.

——————————————————

Step 4: For older versions of WordPress, inside the WP admin panel click on presentation. Then click on the Widgets sub-menu item. If you are using WordPress 2.5 you should click on Design then Widgets.

Drag the Mortgage Calculator and any other needed widgets (categories, archives, links, pages, etc.) into Sidebar 1.

Click “Save Changes” and your Mortgage Calculator should be live.

Can’t see widgets? Your WordPress theme may not be widget aware. To make it widget aware you need to ensure your theme has a functions.php file and that your sidebar is theme friendly. This Automattic page describes how to make themes widget friendly.

——————————————————

Want an easier way to install a mortgage calculator on your site? Perhaps you could try using one of our other linking options – like posting HTML into one of your blog posts.

Have questions, comments, or feedback? Leave them below.

Thank you & enjoy!

Don’t Depend on Social Security Paying Your Mortgage

zFacts published an article about the US National Debt vs GDP

In 1981 the gross national debt, compared to the nation’s annual income, reached its lowest point since 1931, 32.5%. It could have been paid off then more easily than at any time in the previous 50 years. Despite his claim to hate the debt, Reagan instituted unprecedented peacetime deficit spending. This is not partisan politics, this is straight off the White House web site.

Currently about half of the US government’s deficit comes in the form of borrowing from social security:

The gross (total) deficit is bigger because it takes into account that when the fed’s general fund (mostly military spending) borrows money from the Social Security Trust Fund, it will have to pay it back. Borrowing from Social Security is still borrowing. Deficit lite, which Bush is talking about, assumes there is no such obligation — that Social Security will not have to be paid back. So the more they borrow from Social Security the smaller is deficit lite.

President Bush has been lobbying to strengthen social security by privatizing it. Currently the social security system has a surpluss large enough that it helps the government cook the books by over $100 billion a year, but in about 15 years it will start costing the government more than it takes in. When it does that you can guarantee at least one of the following will happen

- sharply higher taxes

- sharply lower social security payouts

- inflation (and rising interest rates) due to greater borrowing and an increasing currency supply

If you are counting on social security paying part of your mortgage you might be taking a big risk. Due to accouning fraud, the government is hiding nearly a half million dollars of debt owed by each US houshold. A recent USA Today article pegged the number at $516,348 per household. What happens to home mortgage interest rates the day we default on that debt?

Mortgage Question: What is a Deed of Trust?

A deed of trust is a special type of mortgage which involves 3 parties.

- trustor: the borrower

- lender: the bank (or other source of financing)

- trustee: the person who temporarily holds the title until you have paid off your lien

When you pay off your debt the deed of trust is cancelled.

How Do Mortgages Compare to a Deed of Trust?

What is commonly referred to as a mortgage, is actually a deed of trust. In fact, 34 out of 50 states use allow home sales via a deed of trust. Home lenders typically prefer to use a deed of trust over a mortgage because it gives them greater legal protection and does not require an appearance in court to have the trustee foreclose and sell on a delinquent mortgagor.

The differences between a mortgage and a deed of trust are

- a deed of trust involves three parties and foreclosure typically is much faster because it does not require going through the court system

- a mortgage only has two parties and foreclosure typically is much slower because it may require going through the court system to get a judicial foreclosure