Changes to the Mortgage Tax Deduction?

Edit: the below blog post was published 7 years ago. We also recently covered the Tax Cuts and Jobs Act which goes into effect in 2018.

A new Congressional proposal would eliminate one of the distinguishing features of a (US) mortgage: the mortgage interest tax deduction. Critics of the deduction have long argued that it deprives the federal government of much-need revenue, that it contributes to home-price inflation, and that it doesn’t do much to spur home ownership. As a result, the consensus is that an alternative system needs to be legislated into existence, and it must be equitable, effective, and efficient.

Towards those ends, the Wyden-Gregg bill, which is currently working its way through the system, would either completely do away with, or scale back the deduction that many homeowners currently claim when filing their taxes. One proposal would impose a maximum income constraint of $250,000 on would-be filers, in order to address the concern that the deduction primarily benefits the wealthy. Another proposal would replace the annual tax deduction with a one-time homebuyer tax credit, amounting to perhaps $10K. Rest assured, however, since the bill doesn’t have much support – given current economic conditions – and it seems unlikely that the deduction will be phased out any time soon.

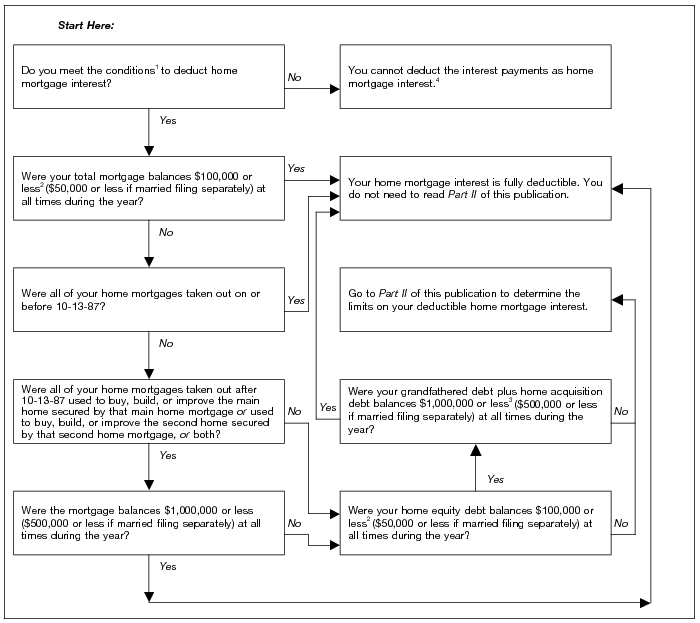

For the time being, then, you can still deduct interest on the first $1 million of mortgage debt, as well as all of your property taxes, for up to separate residences. (That’s $1 million all together, not each). In addition, you can also deduct interest costs on up to $100,000 for a home equity line of credit. For now, you can also deduct private mortgage insurance (PMI), but only if you bought your house in 2007 or later. Property taxes – but not homeowners insurance – are also deductible. As with any aspect of the tax code, the mortgage interest tax deduction is much more complicated than you think, and there are a handful of conditions that must be met before you can claim it. The most important one is that you itemize when filing your taxes. For more information, refer to the IRS website, and review the flowchart below.

If you are in the process of buying a home (and obtaining a mortgage), you can use our Real Estate Tax Benefits Calculator to estimate the savings associated with deducting your mortgage interest. Basically, the calculator will multiply your marginal tax rate by your estimated annual mortgage interest (as well as PMI and property taxes) to determine how much you will save as a result of the deduction. Given the uncertainty surrounding this perk, however, you would be wise to treat the savings as a gift, and not try to apply all of it towards a more expensive mortgage.

El Monte Homeowners May Want to Refinance While Rates Are Low

US 10-year Treasury rates have recently fallen to all-time record lows due to the spread of coronavirus driving a risk off sentiment, with other financial rates falling in tandem. Homeowners who buy or refinance at today's low rates may benefit from recent rate volatility.

The following table shows current 30-year mortgage refinance rates available in El Monte. You can use the menus to select other loan durations, alter the loan amount. or change your location.

Leave a Reply

Free Mortgage Calculator for Your Website!

Would your customers benefit from a free mortgage calculator on your website? Learn how to add a calculator to your website in less than a minute - FREE!